An Important Note for Mobile Users:

To view the complete course navigation panel, please rotate your device to landscape mode.

📖 Course Navigation

1) Introduction

2) Understanding the Deal

3) Passive Investor Due-Diligence

Part 1: People

Part 1: People

4) Passive Investor Due-Diligence

Part 2: Numbers

Part 2: Numbers

5) Limited Partner Due-Diligence

6) Syndication Documents

7) Other Investment Options that are Syndicated

8) Formulating Your Investor Philosophy & Building a Network

9) Venture Capital & Angel Investing

[UNDER CONSTRUCTION]

[UNDER CONSTRUCTION]

BONUS 1 – Syndicator Lies from Real Deals

BONUS 2 – Secrets of Syndication Video Series

BONUS 3 – Understanding Development (Heavy Value-Add)

BONUS 4 – Property Tour Videos

RESOURCE – Syndication Due-Diligence Scorecard & Checklist

The Wealth Elevator Syndication eCourse

Syndication Due-Diligence for (LPs) Passive Investors

Course Homepage | 2) Understanding the Deal | 2.1 Types of Syndications

INVESTOR EDUCATION

What Are the Two Typical Syndication Methods?

Regulation D Rule 506B – 90-97% of deals out there accept non accredited investors as the limited partnership, but the deal sponsor or General Partner (GP) cannot openly market (generally solicit) the syndication deal to a non-private list (for example, no TV, Radio, or social media ads). You can take my word for it (if you value your time) or look it up by randomly looking at all the deals on the SEC website.

Non accredited investors will need to build relationships and demonstrate sophistication to syndicators in order to gain access and learn more about these investment opportunities. Investors (limited partners) in a 506B real estate syndication deal will self-certify if they are accredited or non-accredited.

The SEC limits each real estate syndicate deal to 35 sophisticated non-accredited investors. The law defines an investor as being “sophisticated” if they have sufficient knowledge and experience in financial and business matters to evaluate the merits and risks of investments. In all honestly, no one really knows what the term “sophisticated” means.

Beware: If a syndicator is taking non-accredited investors (especially multiple investors at lower minimum investments of under $25k) it could signal that an operator is desperate for potential investors. A non-accredited individual investor may require a lot of education, the most litigious (because it’s a big part of their life savings), be whiny, and be less of a “returning” investor (i.e., once they go into a few deals, they have deployed all their money).

Don’t come across as a “know-it-all” or total pain ultra-sophisticated investor because a real estate syndicator’s worst nightmare is asking very painstaking questions regarding profit and loss statements every monthly statement. When you get on a plane, do you ask the pilots if they know what they are doing every step of the way once the plane has taken off? We discuss this in the Secrets of Syndications Video Series but for now progress through these first few modules before checking that Bonus section out.

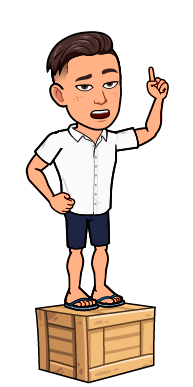

Regulation D Rule 506C – the minority of deals follow the newer rules where you can freely advertise in the world, but the SEC says if you do this, you cannot bring in non-accredited investors. A limited partner will need a third-party letter from a lawyer, accountant, or third-party site like Verify-Investor that validates Accredited status.

Anyone who says “there is no longer a pre-existing substantive relationship requirement and no waiting period” has confused Rule 506(b) with Rule 506(c), the latter of which does allow advertising to anyone, provided the issuer/sponsor takes reasonable steps to ensure that it only accepts funds from investors who are accredited and that their financial qualifications have been verified within 90 days of making the investment.

One of my biggest pet peeves I hear unsophisticated investors talk about when evaluating deals is:

1) What is the real estate syndication structure, and

2) split/fee scheme, is it a straight split?

Passive investors really like to talk about this stuff but in my opinion, it does not really talk about the deal or business plan at all!

I get it… most unsophisticated don’t even know how to underwrite deals or vet the operators so they focus on what they know (so they don’t get embarrassed talking to other sophisticated investors). But from here on out in this course you will see fewer items discussing:

1) What is the syndication structure – 506B or 506C example above, and

2) split/fee scheme and more of what really matters which is the assumptions in the deal underwriting and vetting the business plan.

Conclusion and Key Takeaways

Two Common Syndication Methods Have Distinct Rules – Most syndicated real estate operate under the legal structure Regulation D Rule 506B, allowing non-accredited investors but restricting public marketing. Regulation D Rule 506C, on the other hand, permits advertising but only accepts accredited investors who must provide third-party verification.

Non-Accredited Investors Must Build Relationships – Since 506B syndications allow up to 35 non-accredited but “sophisticated” investors, those interested in these deals must develop relationships with sponsors and demonstrate financial knowledge to gain access.

Low Minimums Can Signal Operator Desperation – Syndicators accepting non-accredited investors, especially at low investment thresholds (e.g., under $25K), may indicate financial struggles or a lack of experienced investors, which could be a red flag.

Sophisticated Investors Focus on the Business Plan, Not Just Fees – Many passive investors get fixated on deal structure and fees rather than evaluating the underwriting assumptions and business plan, which are far more critical to investment success.

Verification Matters for 506C Investments – Unlike 506B, Rule 506C requires accredited investors to verify their status via legal, accounting, or third-party services, ensuring compliance with SEC regulations.

Syndicator-Investor Dynamics Matter – Investors should avoid being overly demanding or combative, as sponsors prefer investors who understand the process rather than those who constantly scrutinize every detail like an airline passenger questioning the pilot mid-flight.