An Important Note for Mobile Users:

To view the complete course navigation panel, please rotate your device to landscape mode.

📖 Course Navigation

1) Introduction

2) Understanding the Deal

3) Passive Investor Due-Diligence

Part 1: People

Part 1: People

4) Passive Investor Due-Diligence

Part 2: Numbers

Part 2: Numbers

5) Limited Partner Due-Diligence

6) Syndication Documents

7) Other Investment Options that are Syndicated

8) Formulating Your Investor Philosophy & Building a Network

9) Venture Capital & Angel Investing

[UNDER CONSTRUCTION]

[UNDER CONSTRUCTION]

BONUS 1 – Syndicator Lies from Real Deals

BONUS 2 – Secrets of Syndication Video Series

BONUS 3 – Understanding Development (Heavy Value-Add)

BONUS 4 – Property Tour Videos

RESOURCE – Syndication Due-Diligence Scorecard & Checklist

The Wealth Elevator Syndication eCourse

Syndication Due-Diligence for (LPs) Passive Investors

Course Homepage | 1) Introduction | 1.4 Syndication Structure

INVESTOR EDUCATION

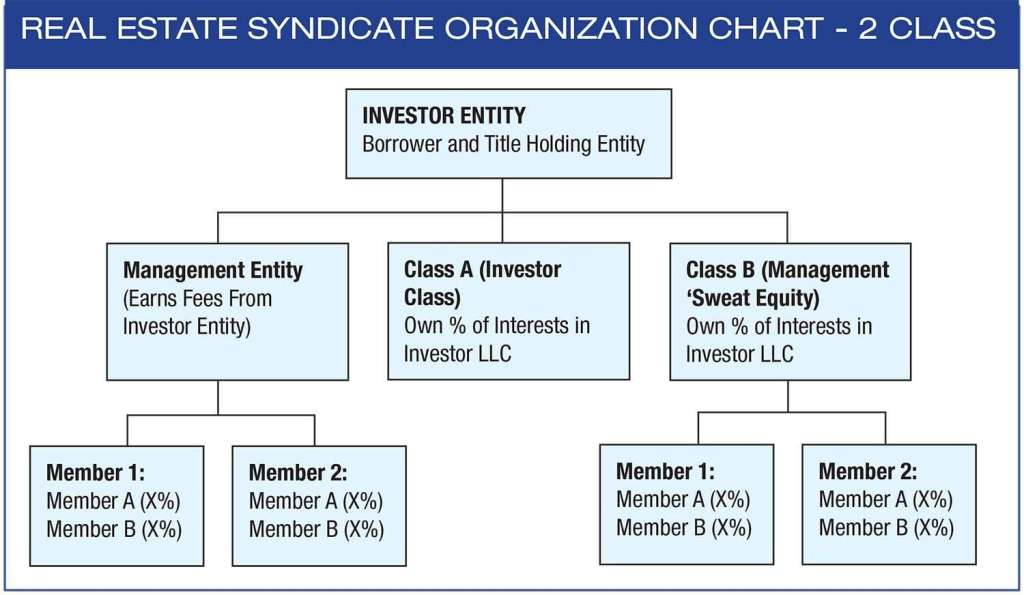

How are Syndications Structured?

There are numerous ways to structure a real estate syndication. The following model describes a typical two-class syndication with equity investors and a separate management entity.

In the above scenario deal structure, a separate, title-holding entity (the “Investor Entity”) that is also the borrower on any bank loan sells interests to Investors.

A limited liability company (LLC) used as the Investor Entity will be “manager-managed” with a “Manager” management entity and “Members” as the passive Investors. Alternatively, you could use a Limited Partnership with a general partner (GP) as the management entity and limited partner (LP) as the passive Investors. For purposes of this article, we will use terminology consistent with an LLC (Manager and Members), as this is the structure most syndicators currently use.

The Investor Entity will need an agreement (the “Company Agreement”) between the management entity (the “Manager”) and Investors (the “Members”) that will govern how the Investor Entity will operate. The Company Agreement will define the Manager’s and the Members’ rights and duties and how cash will be distributed to each of them.

Note: This syndication structure stuff really isn’t too important as LPs should focus on doing due diligence on the syndication deal and people involved rather than worrying too about these legal nuances. Passive investors need to look at the real estate syndication deal holistically and not get bogged down in minutiae. I have seen so many detail-orientated investors who have never jumped into a deal shoot themselves out, get confused, or worse jump into the wrong syndication opportunity because they focused myopically on the wrong thing.

Manager

For the Managers, they would typically use a separate LLC (“Manager LLC”) that includes the management team as its members. If an individual is named as the Manager, the Investor Entity can be harmed if something happens to that person, as it will no longer have a Manager until the Members can elect a replacement.

If the Manager LLC is itself a multi-member LLC, the Manager LLC will continue to exist as long as it has multiple investors, and this protects the Investors because the Investor Entity will remain unaffected if something happens to one of the members of the Manager LLC.

The Manager will earn certain fees for their active role in managing the Investor Entity, including fees such as an Acquisition Fee or Organization and Due Diligence Fee, Asset Management Fees, Refinance Fees, or Disposition Fees. We will talk later regarding what the normal ranges are.

Members

The Investor Entity in a syndicate will typically have multiple classes of Members. We’ll call them Class A (for cash-paying Investors) and Class B (the management or “sweat-equity” class).

If certain Class A Members will have different returns, Class A can be broken into separate sub-classes (e.g., Class A-1, Class A-2, etc.).

Class A

Investors will purchase Class A interests in the Investor Entity and become Class A Members. Class A Members will contribute 100% of the capital contributions necessary to capitalize the Investor Entity in exchange for a portion (e.g., 50%-80%) of its ownership interests. The Manager LLC (or its members) will retain the rest of the interests as compensation for their contributions to the Investor Entity. Both Class A Members and Class B Members will receive “distributions” based on their ownership interests.

Class A Members may be offered a preferred return, meaning they get paid their returns before Class B Members get paid any distributions. Preferred returns can be cumulative ( i.e., accrue even if no cash is available to pay it until some future event) or noncumulative (not as common). Preferred returns are typically calculated on an annualized basis but determined quarterly.

If the preferred return is “cumulative,” arrearages (if any) would be made up at the next distribution event prior to paying current returns. Or arrearages could be deferred until a “capital transaction,” such as a refinance or sale of the property (depending on what your Company Agreement says). In this case, arrearages are paid after refunding Class A Members capital contributions, but before paying distributions to Class B Members or splitting equity between Class A Members and Class B Members. All of this is spelled out in a distribution “waterfall” in the Company Agreement.

If the return is “noncumulative,” Class A Members get all of the distributable cash needed to make up their preferred return for the current distribution period, but deficiencies do not accrue.

When sponsors/GP/syndicators/leads put money into the deal, they are not putting it into the B side (that is not possible) but they are investing in the A side as an LP buying up those units.

Class B

Class B is the sponsor/GP/operator class. This class typically includes members of the Manager and/or others who provide services to the company, as determined by the Manager. Class B Members keep the remaining ownership interests in the Investor Entity in exchange for a nominal amount (usually $100 or $1,000 total) plus their “non-capital contributions” to the Investor Entity. By paying for their interests, Class B Members can establish a cost basis for their investment so that when they do receive distributions, they may be taxable at capital gains rates versus ordinary income rates that would include self-employment tax.

Class B Members only receive their portion of the distributable cash during operations after Class A Members have received their annualized Preferred Returns (if there is a Preferred Return or “pref”). Not to get into the weeds as every deal is different in some cases, Class B Members only receive distributions after both Class A Members capital contributions are refunded and any arrearages in Class A Member Preferred Returns have been paid. Consequently, Class B Members’ returns are subordinate to that of Class A Members. Class A and B members can be paid out at the same time at different ratios, for example in a 70/30 LP/GP straight split deal, profits are sent out 70 cents going to passive investors, and 30 cents going to the sponsor team for every dollar made.

You can’t buy class B shares.

Note – A and B classes can be switched in the naming convention. It really does not matter what you call them or in what alphabetical order there is. It is typical to put LP investors first (make them feel special) which is why most people use “Class A” for the passive investors.

Why Use the Two-Class Structure?

1. To preserve distributions for the management class if the Manager is removed.

2. To segregate fees from distributions so that earnings on Class B Member distributions may be taxable at capital gains rates, versus the Manager’s fees, which will be taxed at ordinary income rates (with self-employment tax on those earnings).

3. Since Class B retains a percentage of the interests, the Manager can allocate those interests as it sees fit amongst persons who provide services to the Investor Entity. This could be useful for people who find deals, participate in money raising, and guarantee loans on behalf of the Investor Entity.

4. From a liability perspective, the Class B side are the Managing Members and first in line of any litigation as they are the decision makers.

In some cases, typically where loan balances exceed $10M, the lender will require a separate, single-purpose entity (separate from the Investor entity) to serve as the borrower and title-holding entity. In such cases, the title-holding entity will be wholly owned by the Investor Entity.

What Are the Types of Syndications/Private Placements?

Open-Ended Fund

Open-Ended Funds are typically offered as an ongoing vehicle where the Fund Manager is constantly buying and selling assets like multiple properties in multifamily real estate for the Fund. Often, these types of Funds offer redemption features so syndication investors can exit the Fund, after a stated lock-up period.

New investors can come into the Fund over time as well. One significant advantage for the potential investor is that they automatically have diversification in their portfolio because their investment into the Fund exposes their capital beyond just a single asset and across all assets the Fund owns. A disadvantage is that the investor has no day-to-day control over the assets in the Fund and is relying solely on the fund manager’s discretion. Cash flow distributions to investors may be made monthly, quarterly, or at different intervals and come in the form of cash to the investor or may be reinvested back to the Fund, depending on the fund’s specific setup.

Closed-Ended Funds

Similar to open-ended funds, typically have multiple assets in them and therefore provide an element of diversification. However, there are typically no redemption options as the Fund is designed to have a finite shelf-life, both in terms of a fundraising period and an estimated deal lifecycle.

The deals the manager selects for the Fund have an expected return which is generally distributed to investors once the deal is fully completed and then distributed to the investor at the close of the Fund. After the Fund is closed, no more deals will be done and hopefully all investors receive their principal and return on investment back at that time. Regular cash distributions may or may not occur depending on the type of assets going into the Fund. If the assets are long-term growth-related assets, such as a motel conversion to affordable housing, there may not be immediate cash flows until the project is completed and rent payments are collected.

Syndications

Syndications are generally structured for the purpose of raising capital to acquire a small number of assets and/or one single asset. These structures are very commonly used for larger value assets, such as multi-family apartment complexes.

Generally, there isn’t diversification, and like a closed-ended fund, it has a shelf-life based on the syndication sponsor’s belief about when the asset will be liquidated and the principal returned to investors. The syndication may or may not offer cash flow over the life of the offering.

Direct Ownership

Direct Ownership provides investors the greatest control over their assets – in that they make all day-to-day decisions. With Funds and Syndications, the investor is relying solely on the manager to make ongoing decisions.

With direct ownership, all of the investor’s capital has full exposure to the asset and therefore doesn’t bring the diversification element. Depending on the type of asset, there may or may not be a current cash flow component. However, it gives the investor the control to fully position the asset to the specification of their portfolio.

These four access points can offer investors many benefits that advance their individual financial freedom objectives. However, the investor must carefully assess those benefits (and risks) and how much investment capital is allocated amongst these access points, as well as the asset, asset classes, and many other components when making private investments.

Conclusion and Key Takeaways

- Syndication Structures Vary – The most common structure involves an LLC with a Manager (GP) and passive investors (LPs), but variations exist, including Limited Partnerships.

- Passive Investors Should Focus on the Deal, Not Just Structure – While understanding structure is useful, investors should prioritize due diligence on the deal and the people running it rather than getting lost in technical details.

- Types of Syndications and Funds – Open-ended and closed-ended funds offer diversification, whereas syndications typically focus on a single or small set of assets with a defined exit strategy.

- Class A vs. Class B Investors – Class A investors (LPs) provide the capital and often receive preferred returns, while Class B (GPs) manage the deal, take on liability, and are compensated through fees and equity participation.

- Two-Class Structure Benefits – This setup protects the management team, allows for tax-efficient profit distribution, and provides flexibility in compensating those involved in the deal.

- Naming Conventions Don’t Matter – Whether passive investors are called Class A or Class B is arbitrary, but typically, LPs are labeled as Class A to emphasize their importance in the deal.