How Rethinking 401k Contributions Can Accelerate Your Passive Wealth

Most traditional advice says to max the company 401k, add money to an IRA, and let it grow tax deferred. That advice is built for people who expect to have less income in retirement (not TWE readers!). Many of the investors I work with are on the opposite path. They are buying real estate, joining private placements, adding cash flow, and will likely have the same or higher income later. For them, pushing all tax liability into the future can slow down wealth building too (see point 3 below).

The Big Idea

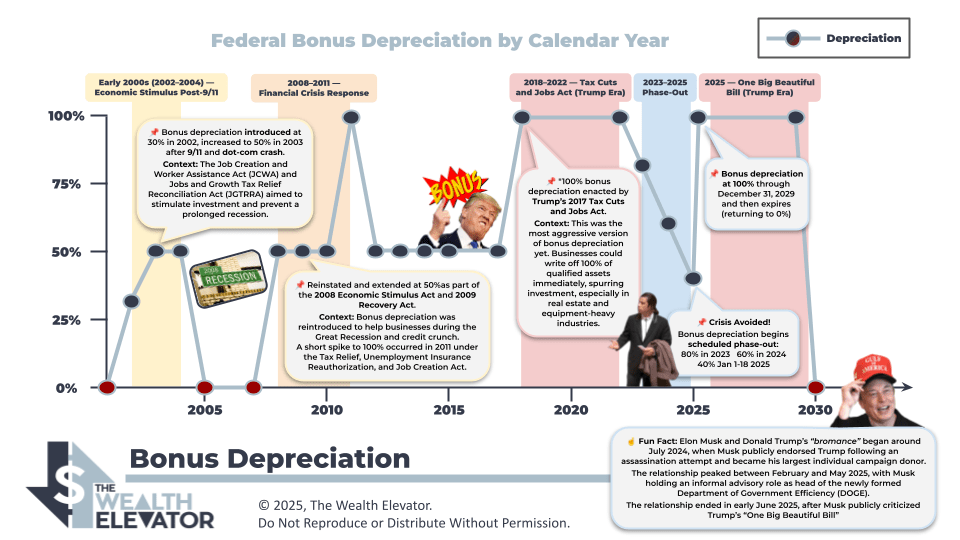

When you defer taxes through a 401k or IRA you agree to pay tax at whatever rate exists in the future. If you believe tax rates will rise, or if you believe your own income will rise, that is not a great trade. A totally separate point is that real estate offers for paper losses through depreciation of the asset and in syndication deals you can augment this by doing a cost segregation and taking advantage of current one hundred percent bonus depreciation. Those tools can create paper losses that reduce taxes today. You feel the benefit right away when the money is invested outside a retirement plan.

Why It Matters Now

Government spending is increasing. Programs for health care and retirement are not getting smaller. Many investors expect tax rates to go up over time. If you defer everything, you may be giving the government a blank check to tax you later.

There is also the timing problem. If you lock most of your capital in retirement accounts, you may need to wait an extra decade to use it without penalties. That is like sending your money to your future self and telling your current self to be patient even though good deals exist today.

Real World Example

I see this pattern a lot (they later come to me in their 50s). A professional in their twenties or thirties listens to HR and maxes the 401k every year. They get promoted. They reach incomes in the four hundred thousand a year range. Along the way in their 40s when their net worth is greater than 1.5M they finally discover real estate syndications and start investing in alternative investments. Then they realize something important. When they try to take money out of the retirement plan, their income is still high. Withdrawals keep them in the top bracket. At that point they tell me they wish they had taken more money earlier when they were in a lower bracket and used it to buy deals.

Now compare that to an investor who used taxable funds to join a large real estate deal. The sponsor ordered a cost segregation study and applied one hundred percent bonus depreciation. That investor received a large paper loss in year one. That loss helped lower taxes on current income. The tax savings could be reinvested right away. That is the time value of money working in your favor. Of course not giving a tax/legal advice so please let us know if you need a referral to 💼 CPA ⚖️ Lawyer or other vendor here.

Mistakes to Avoid

- Deferring taxes without running the numbers on your future income level.

- Assuming retirement accounts are the only safe place for long term money.

- Ignoring the lost benefit of real estate depreciation when investing through retirement plans.

- Surrounding yourself only with coworkers who follow the default script.

How to Apply This

First, take the easy wins. If your employer matches a portion of your 401k contribution, it often makes sense to contribute at least to the match. After that, ask whether every extra dollar should go into the plan or whether some of it should be directed toward assets that offer current tax benefits.

Second, talk with your CPA about using cost segregation and bonus depreciation on real estate investments held outside retirement accounts. Ask how much of that loss you can use this year. Ask how it interacts with your other passive income. If you or your spouse can qualify for real estate professional status, explore that as well.

Third, build a peer group. If everyone around you is doing the traditional plan, you will feel pressure to stay in the box. When you attend events with other accredited investors, you will hear strategies that match where you are headed.

Conclusion

Tax deferral is not bad. It is just not automatically the best tool for every high income investor. If you expect to earn more later, and if you want the tax advantages of real estate to help you now, consider directing more capital outside of retirement plans. Use today’s savings to buy more assets.