2023-2026: Post-Covid Stimulus Era

History Leading up to 2023

I often forget how we came out of the post COVID era as it seems so long ago.

You likely forgot what it felt like to be stuck in your home. A little bit fearful of the unknown – where were you in March 2020?

COVID brought back huge amounts of stimulus into the economy from the US government. This pumped up the stock market and housing prices – combine with the fact that there was a lot of pent up demand in consumer and business spending from bouncing back from the pandemic closures. That volume of fake money (through quantitative easing) dwarfed the 2008 government stimulus.

This is why Inflation went crazy in 2021/2022 hitting as high as 9.1% (4-5x the goal of the FED).

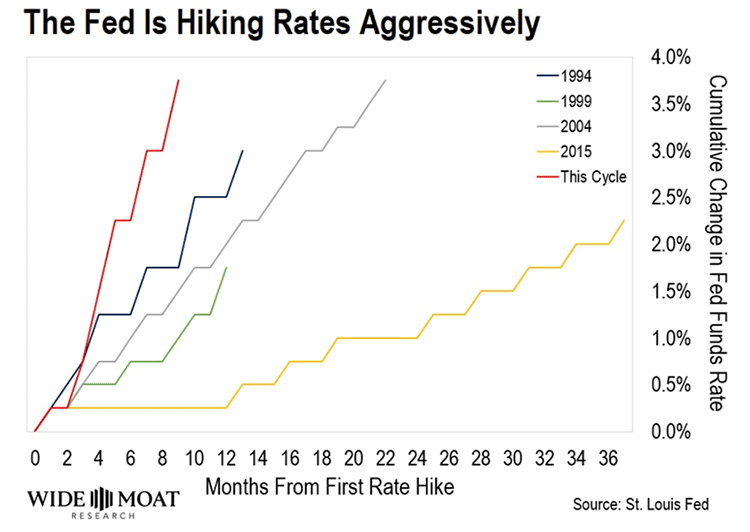

In 2022, the fed, aware of the rampant inflation. Changed the fiscal monetary policy on a dime and switched from Quantitive Easing to Quantitive Tightening.

The barrage of interest rate hikes ensued.

These interest rates hikes were unprecedented. Looking back at the Interest rates hike campaigns of the past these increases were the quickest and most aggressive of the modern era!

This put a lot of stress on the real estate industry who were already facing increasing operating costs (especially on the insurance line item of the P&L due to unprecedented hurricane season in 2019-2022). Those who had floating rate debt (which we had on some deals) saw the interest rate surpass the rate caps that had thought to have been “standard” as an insurance in case of rate increases.

Rents were still going up steadily but expenses were going up higher which created this cash crunch on many operators. Ultimately this ate up the distributions that investors normally would get – still for us as value-add operators the majority of returns come from the refi or sale of an asset which is created by the forced appreciation.

Despite all going on and the reason a lot of us like real estate is that as long as you can pay your debt service, you’re paying down your mortgage, you’re getting your equity buildup. And you can have the ability to wait to sell when the market cycle comes back. You just can’t eat the profits yet… chalk it up to more delay gratification. All the while people’s investment in Crypto and Traditional stock investments pull back.

And that brings us to where we are today.

Real estate prices, I’ll be very careful and I’ll segregate the residential side and the commercial side and speak most notably to the commercial side, which doesn’t always act like the residential real estate market.

As far as the commercial real estate market. The cap rates have increased, which is not a good thing. That means that for the amount of net operating income, you’re getting less of a price for. This is exactly why when we underwrite properties, we assume that the reversion cap rate will increase so we can be conservative assuming that we’re going to be selling in a weaker market in the future.

If this term is new to you check out our Syndication eCourse which you can find the sign up form here.

Many properties purchased in 2021-2022. Have come down in price about 10% in most markets. And in some of the hotter markets, such as Phoenix those prices have come down a bit more, call it 15 to 20%. Its just not a good time to be selling so don’t if you don’t have to because the buyers are holding back, but the buyers are insitutation needing to invest the REIT and lazy retirement plans of Americans so they need to get back into the game at some point not far off. Again, as long as you can stay in the game, cashflow you have the ability to hold for better days and sell in the market cycle and hit your proforma especially if you’re in a value-add project.

On the bright side if you bought during 2001-2022 you weren’t ready to sell anyway because you were not complete with your value add project which typically takes 3-4 years. In other words, it was not time to take the unripened fruit to market yet.

It’s a good time to be stuck in your deal and continuing to value add the property!

Supply/Demand Fundamentals: Growing Need for Workforce Housing

The supply of affordable rental units has significantly decreased over the past decade, with a loss of 3.9 million units nationwide, leaving lower- and middle-income renters with fewer housing options they can afford, as shown in Figure 1 and detailed in the 2023 State of the Nation’s Housing report. Link here.

Right now for apartment owners there is struggle with the increased expenses and floating rate debt. There will be an elevated amount of defaults on commercial real estate deals in the future. Lenders are prepping for oncoming wave of bad loans… and so are we.

We continue to underwrite deals and look for these situations of distress not with the asset but with the owners finances. However combined with where the interest rates are at now we are not seeing anything out there that will pencil to hit our deal criteria. Of course we will let you know when we see something!

Here are some other criteria we are looking at:

- Significant discount from 2022 pricing

- Value add opportunity from a management play (as opposed to physical capital expenditure plan)

- Better locations. Those who struggled were in Class C and lower class B locations.

- Asset class that provide utility and have a growing demand for such as workforce housing. We feel there has been a fundamental shift in the office sector that will take some time to work the supply/demand dynamic out.

That criteria is for our “multi-family” value-add deal zone. Something that we definitely built a track record from in our operational past. But due to economic conditions something that we are holding back on. Side note – this is the area where new operators are always trying to get into and pushing up competition and pricing – in the long term we are trying to leave this sector. Today we have 2.1B in assets and would honestly caution of investing with those under 1B in assets as we were there at one time but for us that was the point where we hired in-house staff who had years of industry experience to play the operator role better than the original founders. We followed the advice of Ronald Reagan – “Surround yourself with the best people you can find, delegate authority, and don’t interfere as long as the policy you’ve decided upon is being carried out.”

We don’t know if there is going to be help coming from the FED or perhaps pressure coming for politicians with the 2024 election coming. However, we need to move and the following is where we pivoted to in late 2022 as we started to see the market shift.

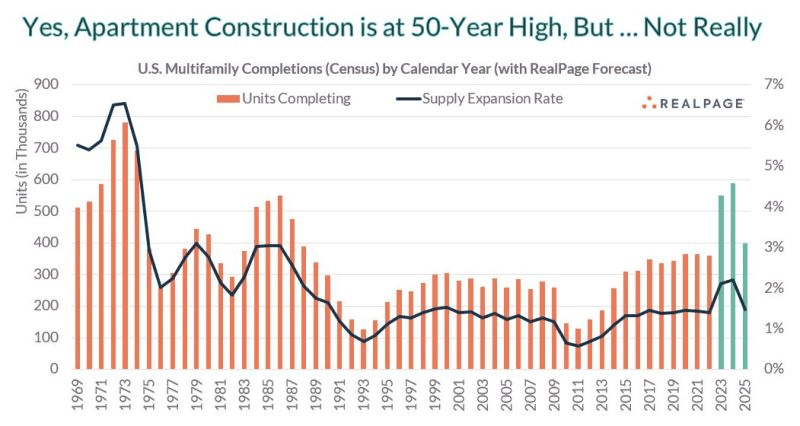

“You’ve probably seen the headlines or heard the chatter: Multifamily construction is at the highest levels in 50 years. There are about 1 million multifamily units actively under construction nationally. BUT to say multifamily construction is at a 50-year high is equally true AND terribly misleading. Why would I say that?

Here are three reasons why it’s misleading:

1) There are roughly 2.5x more multifamily units in the U.S. today than there were in 1970. So that means 1 million units today has nearly 1/3 the impact that it had back in the early 1970s. In other words: The total numbers don’t tell the full story. It’s the relative expansion rate that matters more. At peak, new supply expanded the U.S. multifamily stock by 6.5% in 1973. At peak in this cycle, the inventory expansion rate will measure 2.2%.

If that doesn’t make sense, think of it this way: Let’s say two people get a $6,000 raise. One was making $50k and the other was making $100k. While they saw the same nominal increase, the $50k person’s salary grew at 2x the rate of the $100k person.

2) Multifamily STARTS have consistently come in around HALF the levels seen in the early 1970s. Multifamily starts back then were generally smaller projects that could get approved and built much more quickly than today’s projects do. So that means projects today linger around in the total construction count longer. This is another reason why 1mm units today isn’t the same as 1mm units 50 years ago.

3) Today’s population is much larger than in 1970s — so today’s construction is delivering to a much larger potential renter base. There were 70mm adults between the ages of 25 to 54 back in 1970. Today, there are nearly 130mm. Yes, the 1970s/1980s supply surge benefited from Baby Boomers reaching adulthood. But there are roughly the same number of Millennials, and we never built for them at nearly the same levels — despite the fact that Millennials are often choosing different cities and neighborhoods than their parents did, necessitating the need for more housing in different spots.

Don’t get me wrong: We are building A LOT of apartments. That WILL impact fundamentals, especially these next two years. But I rarely see even industry experts putting the “50-year high” number in proper context. In our view, it’s not the total number at a macro level that is worrisome. We need more housing. But rather, it’s the spots with construction expanding the multifamily stock at much higher rates, like 10%+ in many submarkets and a few markets, especially because most of this construction targets the top quintile of renter household incomes. Demand will eventually catch up to supply, but there will almost certainly be a short-term supply/demand imbalance.

It’s gonna be a tough road for many developers delivering lease-ups in 2023 and 2024. But in most cases, it probably doesn’t compare to what developers in the 1970s and 1980s experienced.”

Jay Parsons

“We are seeing commercial lenders (capital markets) in the market freeze-up. In 2022 Q2, it was the big Fannie/Freddie lenders and 2022 Q4, the smaller community banks started to down volumes as the FED raised rates. Then in March 2023, SVB/First Republic (messed up) opened the door for additional government regulation which meant and even tougher time for borrowers.

Entrepreneurs see the trends in market needs/demands and we want to be in a position to be a bank replacement for operators/developers or even take advantage of overzealous operators in the next 1-5 years (this is called “lend to takeover” method).”

Option One: Preferred Equity

Preferred equity is a type of investment within the capital stack where an investor provides capital to a company in exchange for preferred shares between the common equity and bank loan or debt. It’s a popular investment option amongst higher net worth investors, family offices, Warren Buffet used this to get in on Goldman Sacs in 2008 uncertain times, and institutions because it offers a predictable and stable source of income with priority over other equity investors incase a deal goes south. This means that in case of bankruptcy, preferred equity investors receive their investment back before any common equity investors. However, the tradeoff is that preferred equity investments usually offer lower returns compared to common equity investments.

We have cover pref equity in detail in this section of the ecourse.

In this current environment, pref equity fills the void that has been created by banks pulling back their services. As the one providing said equity it allows for increased compensation due to the shortage. Secondly, with these time of uncertainty we see it as an ideal opportunity to benefit from these higher returns for lower risk while keeping our assets working for us. Plus who does not like monthly income!

Clues in the news: Multifamily Turns to Alternative Financing in a Down Market

“Do you anticipate any of this commercial real estate debacle that is about to hit us affect the PEP fund? Wondering how the macro conditions affect the PEP fund?”

This is the exact reason why we made the PEP Fund as the need for alternative financing (gap funding to long term funding is becoming more of a need) – this will make the PEP Fund be able to negotiate better deals. Plus in the face of economic uncertainty that is why we are opting for pref equity not common equity as we were a year ago in 2021-2022.

Other notes: We are seeing preferred equity investment opportunities from other syndicators that provide annual cash flow of 7-10% and total annual returns of 15-20% that said not all pref equity is the same, you can’t judge a deal or pref equity by the rate of return because every deal is unique and every situation especially as that return goes up has more hair on the deal. Up to this point we have opted for lower risk stabilized projects in the lower end of that spectrum that are not distressed.

In the future we may opt for a more rescue type fund in the future to go after pref equity in deals with more uncertainties in them for a higher return (however unlike the PEP Fund, cashflow will not start from the beginning). But until then we are sitting on the sidelines cherry-picking the lower risk abet lower return preferred equity in clean stabilized deals as well as mitigating our exposure by sitting on top of the common equity.

Option Two: Development

Taking over existing apartments with some cashflow and rehabbing units one by one with a modest renovation budget to bump the rents 100-200 dollar a month makes a lot of sense. Unfortunately, things that “make a lot of sense” creates a frenzy where everyone starts doing it and thus bids up the general pricing for these assets. Secondly, this aforementioned “lipstick on a pig” business plan essentially only minimally increases the value of the asset where the ultimate value-add is ground up development where you take a raw piece of land and turn it into a brand new asset with 60-100+ years of good serviceable life.

Developments, if completed with a competent development firm and professional architect/engineering team can be completed with minimal risk to schedule/budget yet realize the highest amount of profit margin!

Check out our syndication ecourse for the new section on developments for more technical information. In a nutshell, we can build a brand new asset for about 15-25% more than buying a tired old 1980s asset with some lipstick on.

I don’t know if we have seen a better environment for build to rent projects like this. While many people still want an affordable housing – the increased down payment hurdle combined with interest rate hikes – have caused many to put home ownership on hold. Our project fits that niche very nicely. Capital? Obviously, some of the same challenges that potential homeowners face affect us – but at the same time their lack of capital or ability to obtain financing makes our position even stronger because it dampens competition from other builders now and when we do go to market in 2-3 years there will be less supply competing for a growing demand. We are not a big fan of single family build to rent projects since multifamily units are typically more financially viable for builders than single-family units and vastly cheaper when it comes to operation. Also when it comes to operation of apartment units it directly fits within our vertically integrated company function to operate built apartments and be able to wait and sell at the right market cycle whereas most apartment developers are not setup to operate assets as part of their competency.

The downside of developments is the lack of cashflow during the first few years in the build phase but with stagflation now (increase expenses in comparison to increasing rents) there is very little if not any cashflow in even deals that were thought to have been “yield deals” back in pre-2020.

What expenses went up in particular? See video here.

- Most notably 2-3x in insurance costs due to historical losses

- Payroll costs increased by 10-20%

- Taxes increasing year-over-year

- Other general increases due to inflation (see visual example)

Fed calling for a recession as of April 2023 not "soft landing"

Wall of debt coming!

With that said here are other reasons why the movement towards clean developments from multifamily value-add on older (class B and C type tenants):

- Land development deals can be acquired for just $1-3 million, compared to multifamily properties that range from $10-50 million.

- Land development deals can be easily financed with equity alone, making them an attractive investment option.

- In times of high inflation as mentioned earlier, expenses such as property tax, insurance, payroll, and utilities can be difficult to predict for multifamily properties. However, land development deals have almost negligible expenses, making them more predictable and manageable.

- Land development deals have lower expenses compared to older multifamily properties especially in a value add project that has capex or deferred maintenance. This makes developments more resilient to market downturns and a better investment option for turbulent markets.

Action Item: We still believe our country will put through all this recession/slowdown post 2025 so that is why we want to get as many development deals in the 1.5-2.5 year construction funnel now so we are ready to sell when the cycle comes back. When signs are all clear in 2024-2025 will be too late as our competition will start their build phases, we will lose our window.

Recession Plan

We already made movements in 2022 getting ready for the recession and at the very least planning for it or at least few good deals to come in on a one off basis.

Despite to fearmongering media, some economists predicting no recession in 2024:

The March 2023, Linneman Letter discusses the low possibility of a recession in the next 12-18 months. Dr. Peter Linneman argues that although the Federal Reserve (Fed) is trying to create a recession, the strength of the consumer and private sector is preventing it. Recent job growth, industrial output, and low debt service, along with real private wealth above pre-pandemic levels and wages outpacing inflation, are positive indicators. However, the Fed continues to raise interest rates in an attempt to create a recession, which Linneman criticizes, citing recent low inflation rates and supply chain normalization. He anticipates real GDP growth and job growth in the coming years and advises businesses to be cautious during an inevitable recession by conserving cash, focusing on core operations, and improving cost efficiencies. In summary, the Linneman Letter suggests that the strong consumer and private sector performance is likely to keep the economy growing, and the Fed’s interest rate increases are detrimental to the economy, calling for a reevaluation of their strategy.

Of course there are some potential black-swans at play here which tend to never appear (updated as of 4/20/2023):

- Escalating tension in Ukraine – this might help real estate operations as the FED will quickly reverse rates and grossly create stimulus

- Further bank failures despite the past set in March 2023 were not systemic failures of the system but due to poor investment and risk management by the failed banks

- Banks don’t renew a high volume of loan that are coming up for renewals – we are anticipating ourselves and getting ready for this

'Boring' Fundamentals

Too Much for Too Many

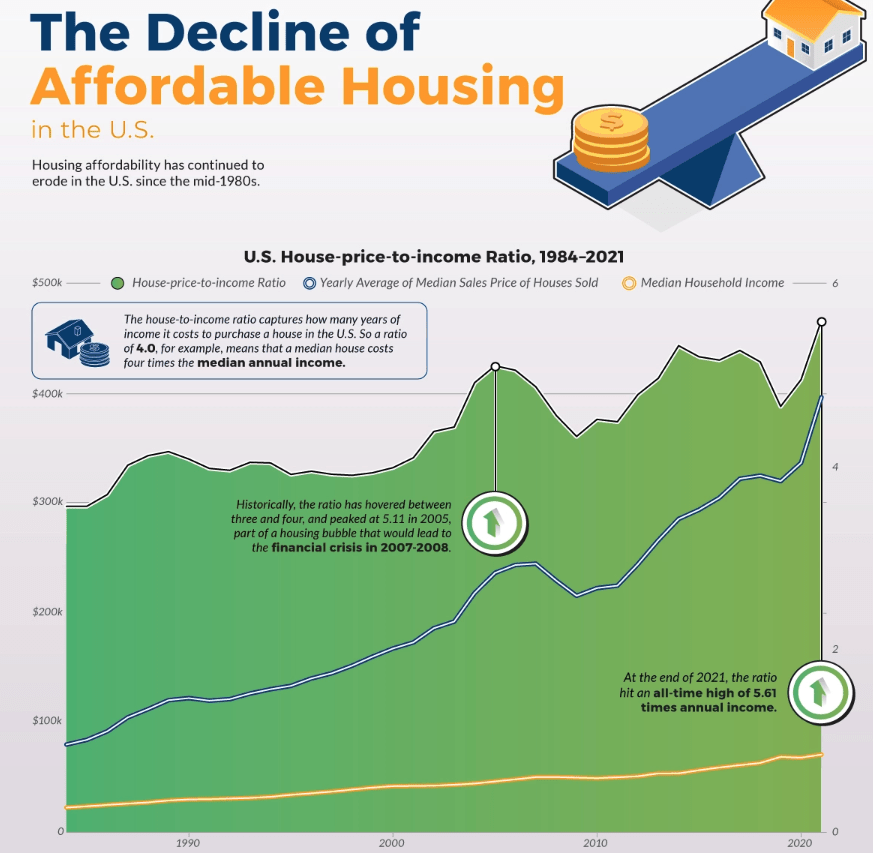

- Housing affordability has fallen to its lowest level in over 30 years. Prices and rents have soared relative to incomes. Spiraling mortgage rates have pushed the homeownership bar further out of reach for a growing share of households. This mid 2023 article cites 4.3 million more homes needed.

- The chronic undersupply of housing is the result of government policies that limit new supply or increase construction costs and is exacerbated by a labor shortage, as well as NIMBYism.

- Simply constructing more housing may be the most obvious and effective solution, but is far from easy to achieve.

With the pandemic and the cascade of economic and social policies it set off, five macro apartment industry tailwinds reached gale-force levels:

- Preexisting multigenerational avalanche of both rent-by-choice and rent-by-necessity demand for multifamily rental units.

- Demand gathered speed and sweep as people sought larger living spaces to balance remote work and household life, and more outdoor living options.

- Constrained construction of new supply, and a price run-up on the single-family for-sale front, spilled over into expanded apartment demand.

- Construction capacity to add new supply stalled as COVID-19 aftershocks played out.

- Compounding the effects of these four dramatic imbalances came the rocket fuel of a global capital rotation toward de-risked assets (i.e., the safe haven of U.S. residential real estate).

- The ability to work from home accelerated the migration.

- Buyers are also searching for the right community. With such high levels of new residents, a CEO of an amenity planning and lifestyle design company noted how amenities played a more direct role in connections. New residents want to be connected—especially via the outdoors—with their neighbors and amenity programming. Lifestyle directors can make an outsized impact in new communities. Her focus for new communities is to make outdoor spaces livable all year long, with heating and cooling elements to make residents comfortable.

- Affordability has played a key role in housing purchase decisions, and the rise in home prices along with higher mortgage rates has brought affordability to the forefront.

“Be greedy when others are fearful

and fearful when others are greedy.”

begin your journey to financial freedom!

My name is Lane Kawaoka, and I hope my blog/podcast will help families realize the powerful wealth-building effects of real estate so they can spend their time on more important, instead of working long hours and worrying about their financial troubles. There are a lot of successful families with good jobs (teachers / engineers / programmers / finance) yet they struggle to make ends meet financially. It is their kiddos who ultimately get the short end of the stick. Being a Latch-Key Child growing up, both my parents had to work and I was left home alone after school to fiddle with my thumbs.

With Real Estate you are able to grow your wealth exponentially faster than the conventional 401K’s and stock investing, therefore you are able to escape the dogma of working 50+ hour weeks at a job that is unfulfilling. And if you are one of the lucky ones who happen to do what you enjoy… well good for you 😛

Money is not everything but it is important because it gives you the freedom to live life on your terms.

Annoyed by the bogus real estate education programs out there (that take money from people who don’t have it in the first place), I set out to make this free website to help other hard-working professionals, the shrinking middle-class. I hope to dispel the Wall-Street dogma of traditional wealth-building, and offer an alternative to “garbage” investments in the 401K/mutual funds that only make the insiders rich. We help the hard-working middle-class build real asset portfolios, by providing free investing education, podcasts, and networking, plus access to investment opportunities not offered to the general public.

“The true meaning of wealth is having the freedom to do what you want, when you want, and with whom you want.

Building cash flow via real estate is the simple part. The difficult part occurs after you are free financially to find your calling and fulfillment.

But that’s a great problem to have ;)”

excerpt from The One Thing That Changed Everything