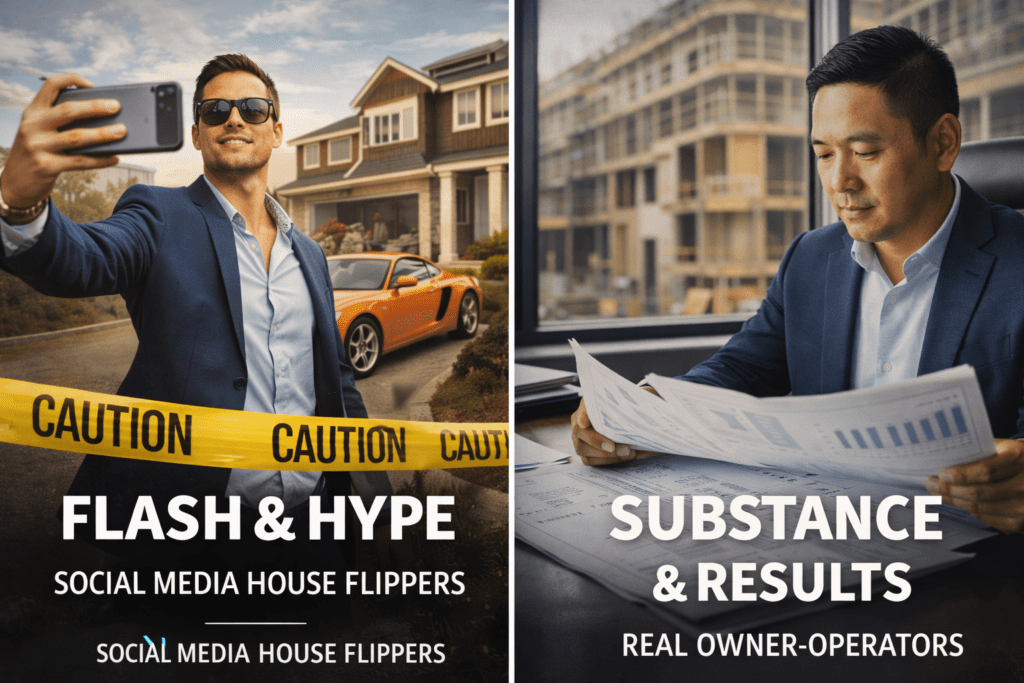

You’ve seen them on Instagram, at meetups, or maybe even in your inbox — house flippers claiming double-digit returns, showing off drone footage, and pitching private lending deals. But here’s the uncomfortable truth:

Many of these “investors” aren’t actually flipping anything. They’re capital connectors — unlicensed middlemen who broker loans, collect a fee, and disappear.

In this post, I’ll break down how capital connectors operate, why they’re risky for passive investors, and how to tell the difference between hype and real operator-backed wealth. I’ve talked on my blog back in 2012 I fell victim to one of those similar traps.

The Big Idea: Capital Connectors Are Not Operators

Capital connectors pose as developers, flippers, or private lenders. But they don’t own the property. They don’t manage contractors. They don’t even sign the loan. Instead, they connect borrowers with capital — often your capital — and take 1–3% in fees upfront.

They vanish the moment the deal funds, regardless of whether it succeeds or fails. That’s not alignment. That’s a liability.

Why It Matters Now

With interest rates fluctuating, inflation compressing margins, and investor appetite shifting toward passive income, the lure of “easy” returns is stronger than ever. Add in flashy marketing and unchecked platforms like Instagram and TikTok, and it’s a perfect storm for misdirection.

Many high-net-worth professionals are being pitched private lending deals by people with zero operational experience — and in some cases, no license to broker loans. One mistake could set your portfolio back years.

Real-World Example: How One Investor Got Burned

One of my clients invested $100,000 into a private flip deal promoted by a capital connector. Everything looked legit online. But within 8 months, the borrower defaulted, and the property was under foreclosure.

The promoter? Already paid and gone.

They had no stake in the outcome and no accountability. That investor is still chasing recovery through legal channels today.

Mistakes to Avoid / Myths to Bust

- Myth #1: “They’re on Instagram, so they must be legit.”

Social media rewards flash, not substance. Always verify who owns and operates the deal. - Mistake #2: Investing based on emotion or personality.

Charisma is not due diligence. Ask for documents. Confirm experience. Vet the team. - Mistake #3: Assuming all lending is passive and safe.

Private lending through unlicensed channels often lacks underwriting and recourse.

How to Apply This

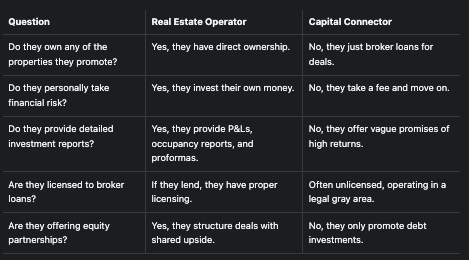

If you’re evaluating a deal, ask the promoter these key questions:

- Are you on title or part of the GP team?

- Do you have equity or are you being paid a fee?

- Can you share the PPM, proforma, and past investor communications?

- Are you licensed to broker loans (if it’s a debt deal)?

- Do you share in the downside risk if the deal underperforms?

If they dodge, deflect, or can’t answer — walk away.

Conclusion

It’s easy to get caught up in the glamor of “fast money” flipping. But real wealth comes from working with experienced, aligned operators who execute with discipline — not hype.

If you’re a high-net-worth investor looking to preserve capital and grow wealth through passive strategies, focus on transparency, alignment, and execution.

Don’t fall for the Instagram illusion. Invest with professionals who are in it for the long haul.

PS check out our syndication guide where you can learn how to do due diligence on the numbers or have us take a look at the numbers with you in our review service.