If you’re AGI is over $300K a year, you’ve probably used real estate depreciation to tame taxes. With bonus depreciation dialing down, many investors ask me what still moves the needle this year. The short answer: oil & gas working interests—when structured properly—can create substantial first-year deductions that may offset W-2 or business income. This post gives you the plain-English playbook, the pitfalls, and a simple model you can take to your CPA. Investing in Oil specifically intangible drilling costs is something that I’ve been doing since 2019 when I went to northern Texas and did my own field trip, there are some actual field videos here. Although personally, I don’t really have a huge tax bill because primarily I invest in real estate which gives you a lot of great bonus depreciation, etc. But for those people with a high adjusted gross income and not doing real estate professional status, this may be your go-to for your tax mitigation.

Section 1 — The Big Idea

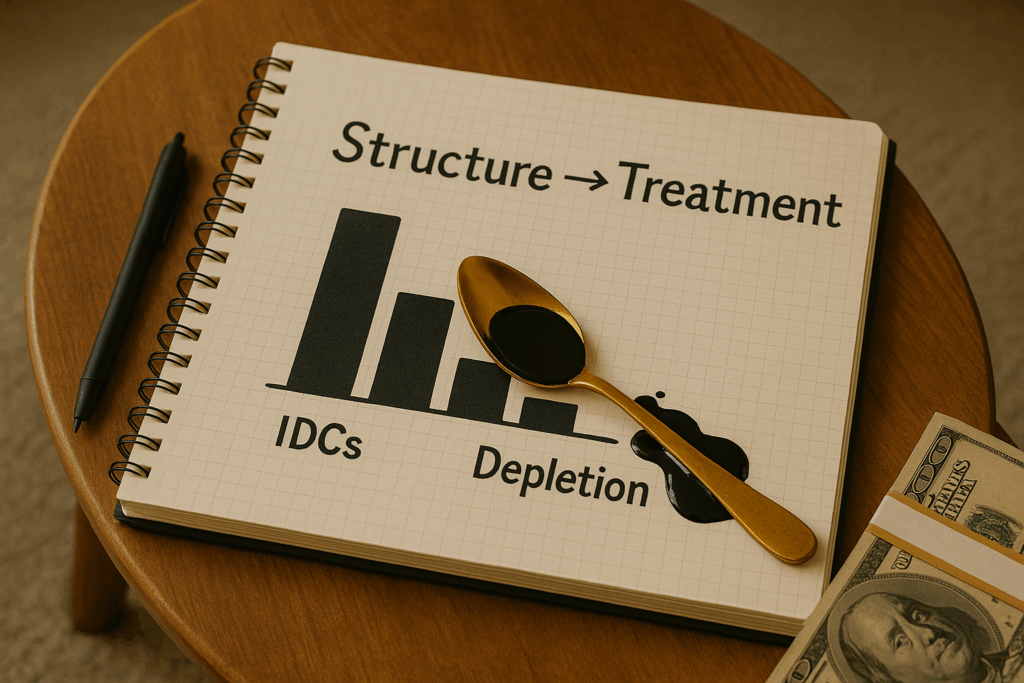

A working interest is a direct ownership interest in a well with no limited liability. Your share of intangible drilling costs (IDCs) is often deductible in year one. If your CPA determines you hold a bona fide working interest, those losses may be non-passive, which is what allows them to potentially offset W-2 or business income. Limit the liability, and you generally lose that treatment—turning losses passive.

Section 2 — Why It Matters Now

Real estate remains great, but bonus depreciation isn’t the one-punch it used to be. O&G provides a different lever: substantial year-one IDCs, followed by production revenue that may benefit from percentage depletion. For high earners trying to solve this year’s tax bill, timing matters.

Section 3 — Real-World Example (Illustrative)

- Allocation: $300,000

- IDC allocation: 65% ($195,000) in year one

- Structure: bona fide working interest (no limited liability)

- CPA treatment: non-passive (investor’s facts & circumstances)

- Result: $195,000 reduces taxable active income this year

- Years 2–4: production distributions; depletion shelters a portion

- Exit: some recapture of prior deductions—modeled up front

Section 4 — Mistakes to Avoid / Myths to Bust

- Myth: “If my K-1 says GP, I’m good.”

Reality: Substance controls. If the docs limit liability, losses are typically passive. - Mistake: Ignoring timing.

Fix: Confirm IDC timing, spud dates, and documentation before year-end. - Mistake: Underwriting the tax benefit, not the wells.

Fix: Diligence the operator: type curves, decline rates, hedging, cost discipline, and capital stack. - Mistake: Forgetting personal limits.

Fix: Discuss at-risk rules and excess business loss caps with your CPA.

Section 5 — How to Apply This

- Ask these questions of the sponsor:

- Does the structure impose limited liability at any level?

- What percentage of my capital is expected as IDCs in year one? How documented?

- What is the development schedule and spud-by plan?

- How are type curves and declines supported? What hedging is in place?

- What’s the plan for exit, and how should I model recapture?

- Ask your CPA:

- Based on my facts, will this be treated as non-passive?

- How do at-risk and excess business loss limits apply to me?

- What’s the plan if my losses carry forward?

- Portfolio fit:

Use O&G as a targeted tool alongside real estate and equities—aimed at near-term tax needs with real-asset exposure.

Conclusion

Oil & gas working interests aren’t magic. But when the structure fits and the operator executes, they can be among the most efficient tools for high-income professionals to reduce taxes in the current year—while building a cash-flowing sleeve with ongoing tax benefits.

Additional video on due-diligence https://youtu.be/ii165-8HDLU?si=51F3VqozCvnBNKe0

Additional research: Oil and gas working interest investments offer unique tax advantages, most notably the deduction of Intangible Drilling Costs (IDCs) in the year incurred, as outlined in Section 263(c) of the Internal Revenue Code. These deductions can significantly offset ordinary (W-2) income, provided the investment is held as a direct working interest—not through an entity that limits liability, such as an LLC or partnership. The IRS specifically addresses this exception in Treasury Regulation 1.469-1T(e)(4)(i), which states that income and losses from direct working interests are generally treated as non-passive, enabling high-income earners to maximize their tax benefits ([IRS Pub 925], [Instructions for Form 8582]). It is crucial to understand the risks and nuances inherent to these investments, including potential recapture at the time of sale and the application of material participation rules. For further reading, consult authoritative tax sources such as Moss Adams’ recent analysis of oil & gas deductions, guidance from experienced real estate CPAs, and educational resources on working interest exceptions. As always, investors should consult with a specialized CPA to ensure compliance and optimal strategy.

If you want to go deeper, reach out Lane@theWealthElevator.com or give us a call 808-215-5531.

Disclaimer: For education only—this is not tax or legal advice or offer to sell securities. Consult your own CPA/attorney. Please let us know if you need a referral to 💼 CPA ⚖️ Lawyer or other vendor here.