Intro

If you are like many busy professionals, most of your investable dollars sit in public equities with a bond fund on the side. That worked fine when money was cheap and markets climbed steadily. The last few years reminded me that concentration feels great on the way up and awful on the way down. In this post I share what I learned by studying how stable families allocate capital using the UBS 2024 single family office survey as the anchor. I am reporting survey findings, not giving allocation advice. The payoff is a simple way to think about your mix so drawdowns feel manageable and decisions get calmer.

The Big Idea

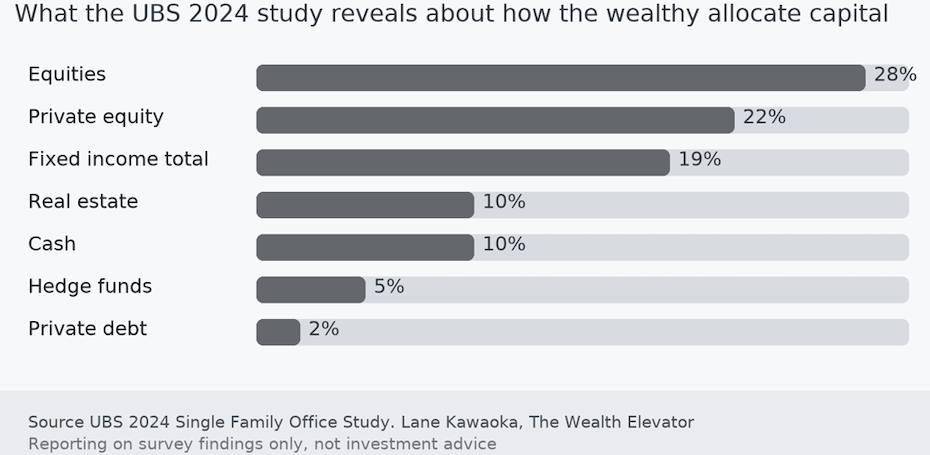

Give every dollar a job. Families in the UBS survey do not rely on one engine. Their average mix looks roughly like this, summarized from the report.

| Asset | Approximate Allocation | Role |

|---|---|---|

| Public equities | About 28 percent | Growth with a tilt to the United States and home region |

| Private equity | About 22 percent | Ownership and control through direct deals and funds |

| Fixed income total | About 19 percent | Paychecks and ballast, includes about 16 percent in developed market bonds |

| Real estate | About 10 percent | Income and tax angles |

| Cash | About 10 percent | Flexibility and opportunity |

| Hedge funds | About 5 percent | Diversifiers |

| Private debt | About 2 percent | Income and niche exposure |

| Smaller sleeves | About 1 percent each | Infrastructure, art and antiques, gold or precious metals |

In total, alternatives are about 42 percent and traditional assets are about 58 percent. About 78 percent of these families plan to invest in generative AI in some form. Reporting survey data only.

Why It Matters Now

Rates are higher than the last cycle. Inflation is sticky. Leadership in public markets rotates quickly. A one engine plan can swing your net worth more than your stomach allows, which tempts reactive moves and tax mistakes. The families in the survey appear to use multiple engines on purpose. Fixed income pays you to wait. Ownership through private equity lets you shape outcomes. Cash near 10 percent lets you act without selling at the wrong time.

Real World Example

Assume two investors with one million dollars each. Investor A has eighty percent in public stocks. Investor B uses a mix that resembles the survey with about 28 percent in public stocks.

If public stocks fall 20 percent in a rough quarter, the math on the public equity sleeve looks like this.

- Investor A loses 0.80 times 20 percent which is 16 percent of the entire portfolio, about one hundred sixty thousand dollars before other sleeves move

- Investor B loses 0.28 times 20 percent which is 5.6 percent of the entire portfolio, about fifty six thousand dollars before other sleeves move

This is not a forecast. It is a reminder that concentration amplifies swings and emotions.

Mistakes To Avoid

- Letting public markets define your entire identity as an investor

- Treating fixed income and cash as leftovers instead of tools

- Buying private deals without underwriting the operator and your own liquidity needs

- Rebalancing only when it feels good, which is usually the wrong time

How To Apply This

- Write a one page roles policy. Define ranges for growth, income, ownership, and liquidity, plus a rule for rebalancing

- If you pursue private placements, underwrite the operator first, the deal second, and your liquidity third. Ask for references and how they handled their worst deal

- Keep a cash floor and a cash ceiling so you can act without forced selling

- Coordinate with your CPA on depreciation and K1 timing, and with your attorney if trusts or entities are involved. If you need a referral use this link.

Conclusion

You do not need to predict markets to build a calmer plan. Decide that every dollar must have a job. Fund multiple engines. Rebalance by rule. If you want next steps, explore related articles here on the site or my masterclass that breaks the journey into clear floors.