Buying or Renting: The Biggest Inhibitor to Financial Freedom?

For the longest time, owning a home has been part of the American dream. This financial decision may seem to be very appealing and highly marketable, but should you buy or rent a house?

Or you are simply being influenced by your real estate broker or close-knit friends surrounding you?

Introduction

In the minds of many, it represents security, stability, and financial independence. Renting has traditionally seen as throwing money away, as many people also see homeownership as a financial investment in their future thanks to the popular belief that properties will only ever rise in home value.

So should you buy or rent? Every individual has different personal finance circumstances that determine if home buying or renting their home is best for their financial situation

Must Watch! He realized that it was a mistake to buy his own home…

What do I do?

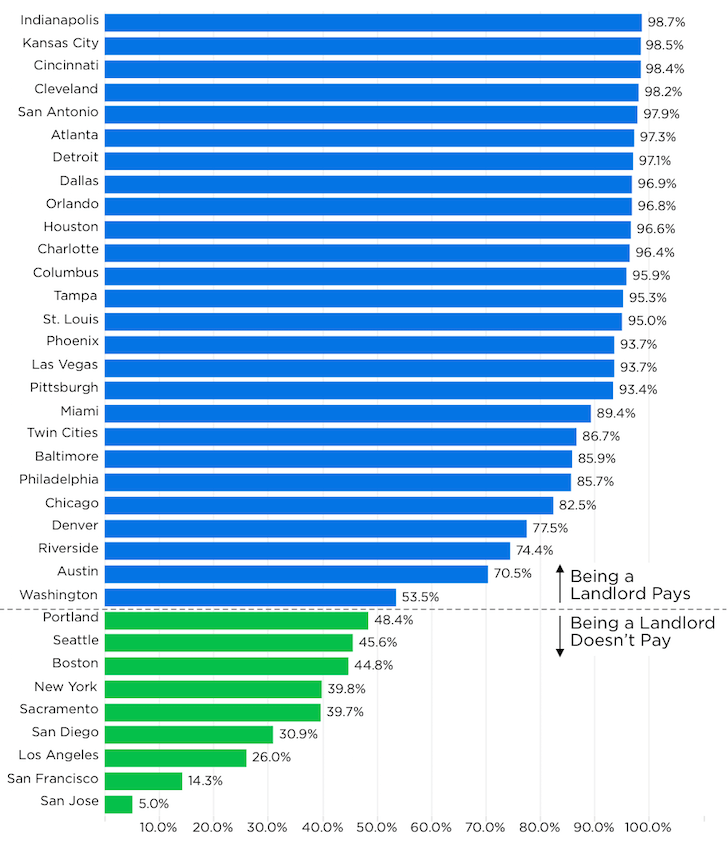

I live in Hawaii where renting a $1M home for $3,000 a month makes more sense. My landlord is making only 3.6% on their money and that does not include any taxes or capital expenses!

Where I get to live in a great home and put my money into buying all these apartments that are kicking off cash flow, so I can reduce taxes, earn appreciation with leverage, and my tenants are paying down my principal payments.

Let me guess you’re thinking, “It’s a property. You are building equity property value will increase over time anyway?”

Yes, home price can go up and appreciate but I consider that gambling.

Sophisticated investors look at the Rent-to-Value Ratio and look for at least 1% or more to be able to cash flow after expenses.

What’s in this guide?

This guide will cover everything you need to consider about purchasing a home, renting, and purchasing a property to rent. This includes:

- The advantages and disadvantages of renting

- The advantages and disadvantages of buying

- The costs associated with renting vs buying

- Choosing a property

- Taking on a home loan

- Using your home to finance your future

- Buying a property to rent

If you can’t save money to save your life then buying a home acts as a forced savings account, which will benefit you in the future.

Rent or Buy? What To Consider

Renting

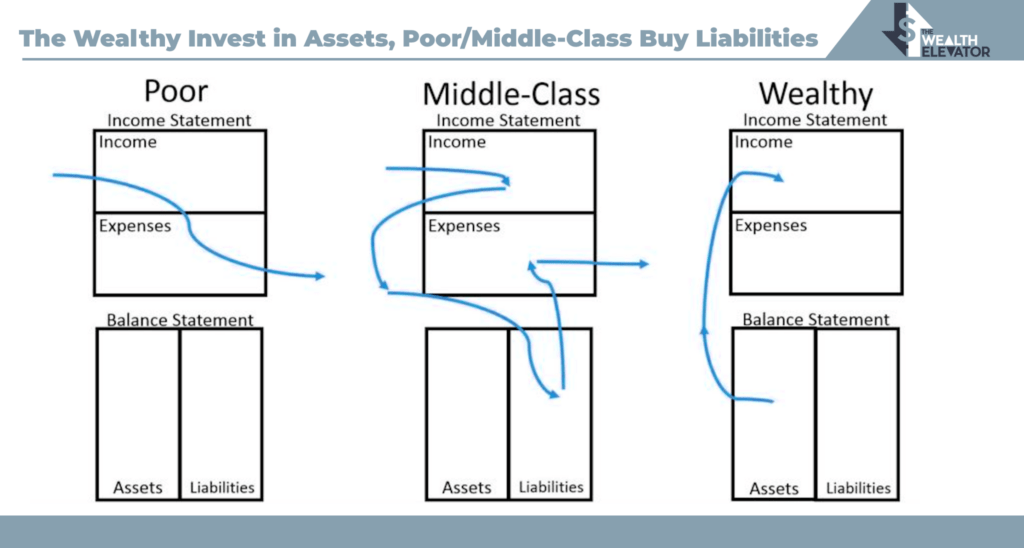

The wealthy do not believe that renting is like flushing money down the toilet but see housing as just another line item in their personal finances.

Advantages of renting:

Flexibility and Mobility

If you decide you don’t like the property/neighborhood, your commute is too long, or that you want to get your kids into a better school district, renting allows you to easily pick up and relocate

Liquidity in Difficult Times

Perhaps your income goes down, unexpected bills occur, or your mom falls in the shower and can’t get up. The beauty of renting is that if your financial circumstances change, you have the option to move somewhere more affordable.

Credit Ratings

Experts estimate that around a third of all American adults have a credit score below 601 and are considered a poor or bad risk. This greatly reduces the likelihood of qualifying for a regular home loan, meaning that borrowers would have to pay higher mortgage interest rates making buying unfeasible.

Buyer’s Remorse

A survey by Trulia found that 44% of American homeowners had some form of buyer’s remorse, with renting if you’re not happy, you’re free to move at the end of your lease term.

Local Costs

If the area you live in has high property taxes, high insurance costs, or low rent-to-value ratios, then the math on renting makes financial sense.

Disadvantages of Renting

Of course, while there are many advantages to renting, there are also drawbacks.

Not Feeling at Home

Tenants are rarely allowed to decorate the property the way they would like. Décor is usually neutral and can feel clinical.

Rent Increase

In some areas, rent increase is limited by local regulations. In most instances, the landlord is free to increase it by as much as they like.

Lack of Security

While renting offers flexibility, it also lacks security. Your landlord might decide that they want to sell the property or have someone else live there.

Lack of Tax Breaks

Home buyers brag about claiming extra tax write-offs on their mortgage interest against their tax bill.

The tax benefits that you get as a real estate investor will blow the mortgage interest tax deduction out of the water.

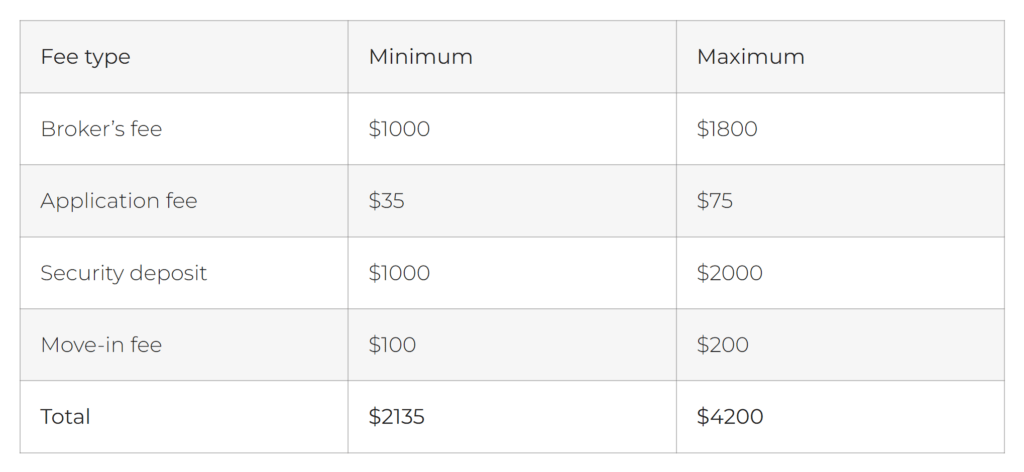

Additional Costs

- Broker’s fee: whether or not you need a broker will depend on where you want to live. In many big cities, landlords or property managers frequently won’t consider any applications that haven’t come through a broker. Typical fees vary between one month’s rent and 15% of the total annual rent. However, this is not the case in most circumstances but I’m just trying to be a good journalist here.

- Application fee: this covers the upfront cost of credit and criminal background checks. Usually cost between $35-75 per person.

- Security deposit: we’ve already mentioned this, and it’s generally set at one or two months’ rent. However, some property types, especially condominiums, charge a move-in fee as well. This covers the charge of updating mailboxes, reprogramming buzzers, etc. This can range from $100-$200.

Based on a $1,000 monthly rent:

What About My Furry Friend?

Many rentals will charge a cleaning fee or surcharge for a pet. Landlords are becoming more accepting of our four-legged friends. In fact, many landlords including myself see your pet ownership as a sign that you are more of a dependable long-term tenant.

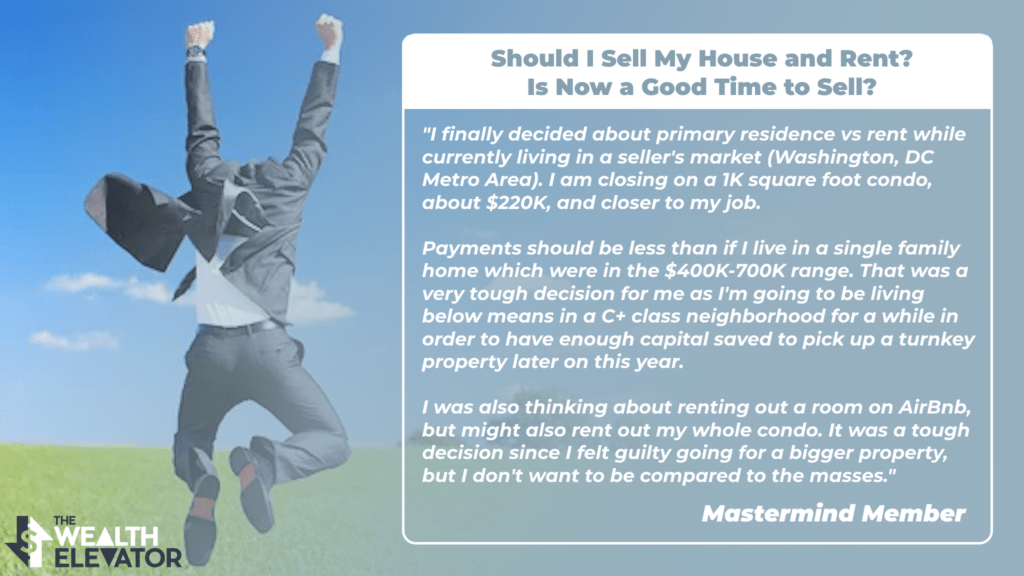

But what if my spouse wants to buy our own home?

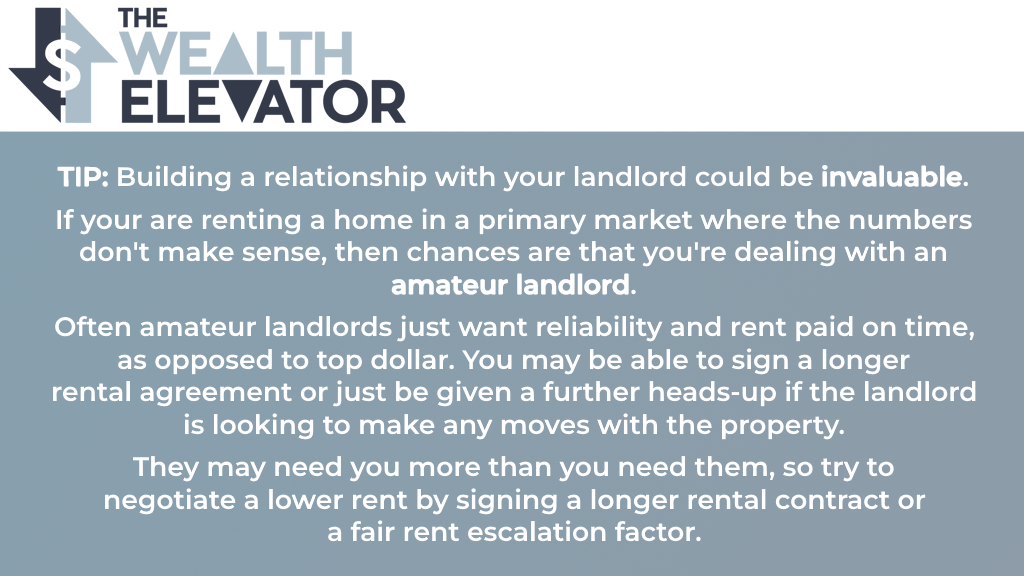

If you are in a primary market the prevailing market rent-to-value ratio under 1% usually means that if you are renting you will be able to live in a much nicer home than if you bought, assuming you had the same PITI mortgage payment.

Say you are looking at a $1,600 mortgage on a $350,000 home (typical 20% down payment). Now consider taking that same $1,600 monthly payment you will be amazed that you would be able to live in a nicer home. This does not even take into account the hidden costs of homeownership that you can dive in with the accompanying spreadsheet.

And by the way, have you ever driven a rental car? It’s a lot more fun when you are not worried about a dent or paint chip here or there.

Purchasing a Home

Now we’ve looked at the pros and cons of renting, we’ll do the same for purchasing a home or property, what to consider when taking out a mortgage, and how your home could be used to finance purchasing a property to rent.

A home is somewhere you live, where you invest emotionally as well as financially. A property can be anything from a piece of land to a luxury penthouse and is purchased as an investment.

While home ownership is usually associated with stability and security to many, that stability and security can be a double-edged sword if your circumstances change.

Being tied into owning a home can restrict where you can work and, therefore, your earning potential.

The Advantages of Home Owning

- Depending on the area, mortgage repayments can be lower than renting.

- Unlike renting, you can live there as long as you like as long as you make your monthly payments.

- A fixed-rate mortgage means that your monthly cost are predictable.

- The interest and property tax on the mortgage are tax deductible. Note: BS Flag!

- For those who struggle to save, a home is a forced savings plan.

- The value of the home may appreciate

- You have an asset you can sell or refinance if you need access to cash.

The Disadvantages of Home Ownership

- It’s a very long-term financial commitment.

- The monthly payments may not be cheaper than renting. Purchasing a property requires a down payment plus considerable closing costs. Money today is more valuable than in the future especially if you can invest and make 10-20% per year.

- Any maintenance and repairs are your responsibility.

- The value of your home may fall.

- You can have terrible neighbors.

- If your life circumstances change, e.g. your wages fall and you can’t afford the mortgage, then you’re stuck in the situation until you’re able to sell.

What to Consider When Taking on a Mortgage

The vast majority of people purchasing a property, whether it’s for their own use or renting, will need a mortgage. A mortgage is a long-term commitment, typically thirty years in the USA.

Mortgage lender typically require a 20% down payment, which immediately reduces your available funds. Even though the high level of competition in the housing market means that interest rates are generally competitive, mortgage payments are still a significant chunk of your income.

If you are also a real estate investor looking for additional income be mindful that one of the biggest factors in getting a loan is the debt-to-income ratio. Having a large mortgage (loan) without the income coming in from your primary residence will greatly impact this ratio.

The History of a Mortgage

The majority of homeownership in the United States is mostly a recent phenomenon. Until the mid-1940s, most Americans did not own their places of residence.

Big banks and their activities could be argued to have been the catalyst for the “American Dream” of homeownership becoming the majority statistic post-1950. The National Bank Acts of the 1860s kick-started this gradual change. US Treasury securities now backed the US National Currency and standardized practices of US national banks. And by the 1890’s, American banks saw the popularity of Mortgages rise.

These early mortgages at the turn of the 1900s were in stark contrast to those that we see today. A typical homeowner in 1916 would pay up to 50% down with a 5-year interest-only structure whereas a typical homeowner will save for 20% with the standard 30-year plan.

Amortized interest front-loads the fees and interest at the beginning of the terms and greatly advantages the bank instead of the homeowner.

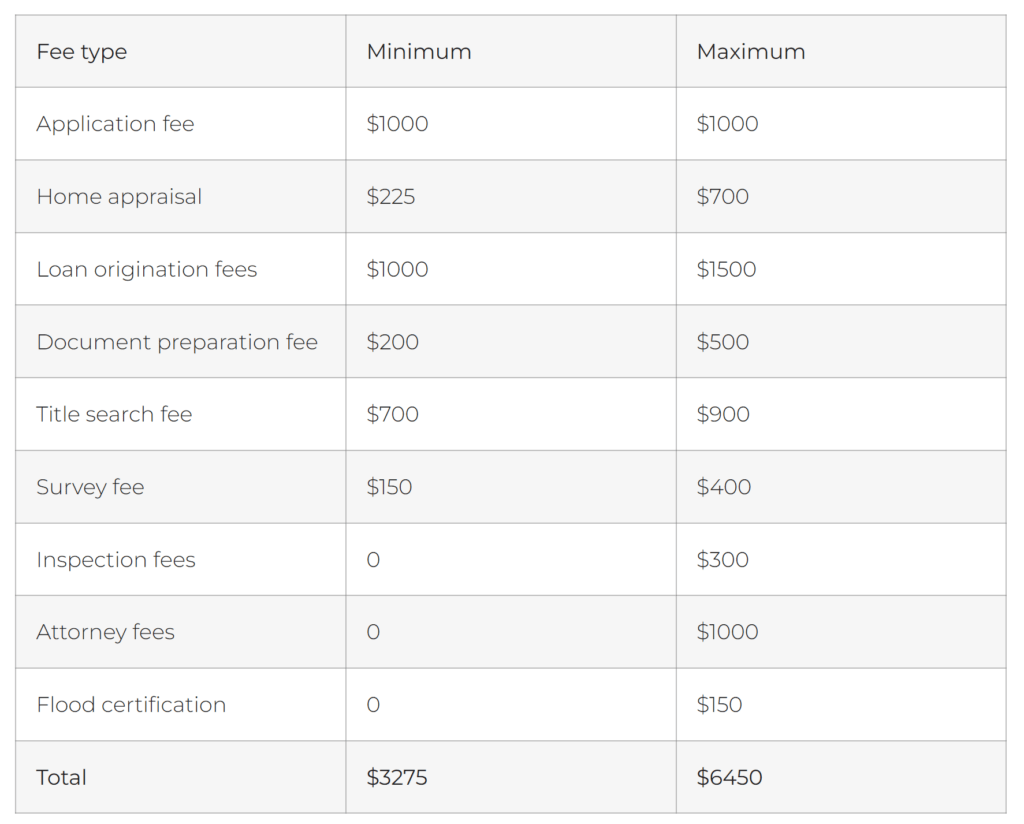

Fees on a $100,000 mortgage:

These are all in addition to a 20% down payment.

While these costs may be negotiable to an extent, they still add up. It may be possible to roll the costs into the loan, but will then attract interest alongside the capital amount, and may push up the interest rate.

Using Your Home to Purchase Other Properties

Another way of purchasing other properties is to use the equity you’ve built up in your home. This can be done by a complete refinance of your home or you could consider taking out a HELOC.

HELOC stands for ‘home equity line of credit’ or, more simply, ‘home equity line’. In some ways, it’s similar to a mortgage, as it is a debt secured against your property. It differs from a mortgage in two significant ways. These are:

- A home equity loan (mortgage) is a lump sum, paid at once. A HELOC allows homeowners to borrow or draw money on multiple occasions usually over a period of 5-10 years, as the need arises, up to a maximum amount.

- As mentioned above, a home equity loan usually has a fixed mortgage rate, while a HELOC normally has variable interest rates linked to Bank Prime.

Advantages of a HELOC

- HELOCs are a convenient way of funding one-off needs, such as a down payment on a second property, or renovation.

- Interest is paid only on the sum borrowed, and during the drawdown period, borrowers can repay just the interest.

- Upfront costs are very low. The cost of taking out a $150,000 HELOC loan is typically less than $1000 and may be paid by the lender without a rate adjustment.

- Some HELOCs can be converted into fixed-rate loans when a drawdown is taken.

Disadvantages of a HELOC

- HELOCs are adjustable rate mortgages (ARM) but are much riskier than a standard ARM thanks to the way the interest is calculated. If the interest rate increases on 30 April, then the HELOC rate will rise on 1 May. There are also no interest rate caps.

- Ensuring that the HELOC is repaid can require considerable financial discipline, especially if the capital must be repaid at the end of the drawdown period.

Buying a Property to Rent

As fewer people are buying their own homes, there is a strong demand for rental property across the country. This demand has been fueled by factors such as the 2008 economic crash, the high number of people with poor credit ratings, stagnant wages, rising purchase price of homes, and the increased mobility of the workforce.

Owning one or more rental properties can be a good investment in your financial freedom. But it requires careful consideration. It’s not like buying a home. When you buy your starter home things like space, schools, and amenities will be your primary focus, and you’re likely to spend more to get your perfect house.

When choosing a rental, you need to look at the local market. Check with a local real estate agent for what types of properties are in demand and choose accordingly. Buying in the best locations with the best school districts will lead to more competition and overpaying for the asset and its rental income stream.

If you do your homework, buying a property to rent can be profitable over time. It’s a way of generating a passive income, while also building up savings through increasing the equity in the property. In many cases, renting will cover the mortgage and the taxes, if not generating a small profit on top.

Renting Out Your Home

Should you want to relocate or want to improve your cash flow, renting out your own home is a possibility. However, this option comes with a number of potential complications – both financial and emotional – that need to be considered.

Financially, you’ll need to inform your mortgage company when your home stops being your residence. Different mortgage lenders have different rules for borrowers who convert their homes into rental properties. It’s common for them to require you to live in your home for at least two years. Typically, mortgage rates for buy-to-rent properties are higher because of the increased risk to the property, and you may need to refinance.

Factors to Consider When Buying a Property to Rent

Just as with deciding whether to rent or buy your home, deciding where to buy to rent needs to be carefully considered.

Rent-to-Value Ratios

The Rent-to-Value Ratio is a quick calculation real estate investors run to determine if a property will cashflow. Take a $100,000 home that rents for $1,000 a month, the Rent-to-Value Ratio would be 1% ($100,000/$1,000). In some areas, such as Seattle, Los Angeles, and the East Coast, properties are expensive to buy, but rents are relatively low. In these areas, rent-to-value ratios can be less than 0.75%, meaning that there is little chance of even covering the costs, making purchasing a property a poor decision. In areas where housing is cheaper to buy and rent-to-value ratios are much higher, then it makes sense to purchase a property and rent it out. In some markets, you can find these Rent-to-Value Ratios over 1.5% in solid areas.

Location

In real estate, the mantra is ‘location, location, location’, and that’s just as true for rental properties. Getting the location of the property right is just as important as choosing the right property type. If the market wants apartments in the city and large houses in the suburbs, buying an apartment in the suburbs could be a costly mistake.

Closing

We skimmed the surface on rental properties. For more information please visit theWealthElevator.com and check out our podcast.