Looking for a good CPA or SDIRA Vendor?

If you would like a referral to the teams that we use please click this button, complete the form, and we will be in contact with in 2-3 business days.

“I created a couple LLC’s for my IRAs (one traditional and one Roth) for investments in syndications.

I talked briefly to my CPA today, and I think I’m throwing in the towel and canceling all my IRA’s. Or at the very least not contributing to any of them anymore today!

The cost of money (LLC’s annual fees, XYZ of SDIRA Custodian annual investment fees, the 990-T income tax returns) and time and energy eat up too much of the profit, and are too time consuming to make the syndications in SDIRAs make sense for me.

I’m still trying to think if there are other investments I can make with this cash that does not involve the leverage, but I will most likely just suck it up and put it back at Vanguard in crappy index funds, and try to pull it out as I can over the next few years without getting into too high of a tax bracket.”

– HUI Investor

Over it with QRPs

It’s a tax-sheltered investment vehicle that you can invest in pretty much anything (real estate, private equity); where your money grows tax-free but it is intended for retirement, and the downside (why I don’t do one personally) is that you can’t touch the money until you are old ☹️

If you have a 401K or Roth or IRA you need to start using a Solo401K or SDIRA.

If you are late to the game of investing in alternative investments like real estate (imagine that), and already have a large 401K over $500,000, then you should convert it to a Solo401K or Solo401k Roth version. At that point, you can slowly take money out to minimize your taxes (not go into the highest tax bracket), and invest in the meantime as you “leak” the money out of the Governments control.

I am very against 401Ks, because you can only choose from crappy option that have heavy fees.

I don’t really like Self Directed Roths or any tax sheltered retirement accounts either, because you are subject to UDFI (more details below) and cannot leverage your investment, which is a pillar in real estate investing. Knock yourself out… but I cashed out mine a while ago, because I plan to live off my cashflow and retire well before the Government allows you to tap into your retirement account.

If you have distrust on where this country is going, you need to expect that taxes will go up in the future. How else will we pay out for all these bank bailouts and quantitative easing?

You will pay taxes, now or later, and you are likely to pay more taxes in the future because you will make more money… so pay it now. Most people think they will be in a lower tax bracket in the future, because they plan to downgrade their lifestyle. This is, again, one of those incorrect money myths that are so prevalent.

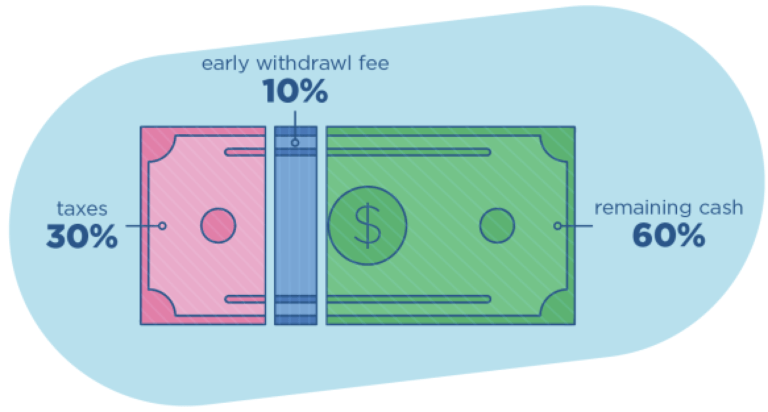

By taking you money out early you will incur a 10% penalty, but if you understand how you can easily get 20-30%+ returns in real estate a year, that 10% penalty is nothing. You can recoup that in 6-18 months.

It’s a no brainer… the numbers don’t lie. Do the math.

Yes, taking money out of your retirement account is a sin for most people.

Just make sure you don’t buy jet skis, and put it in cash flowing assets like rentals or syndications. Or start a business, if you are exceptional at business.

"Retirement accounts (with so-called tax benefits) only make sense if your AGI is over 380k AND you have a substantial amount in your IRA already (400k+). The wealthy people I meet don't use these things as a primary wealth building tool, because it does not help them on their taxes today. These retirement accounts are tools to be used in certain situations."

Lane Kawaoka

Unless you are age 59½, fired, die, or leave your current employer, your company sponsored/owned 401(k) are stuck where they are.

In-service withdrawals can be made as a hardship withdrawals if the plan allows, if there is an “immediate and heavy financial need” per the IRS. Straightforward examples of these are: medical care expenses, educational costs, and payments needed to prevent eviction from a principal residence. You just need to be able to explain how you exhausted all other distributions or nontaxable loans under the plan.

You can only take out the employee’s elective contributions. The income or the money that you made can’t be taken as a hardship withdrawal. If the plan allows, the employer’s matching and discretionary contributions can be factored into a hardship calculation.

Most withdrawals will have a 10% early withdrawal penalty, however, the 10% premature penalty tax can be waived if the in-service withdrawal or hardship distribution is used to cover medical expenses that exceed 7.5% of adjusted gross income (AGI), or if it is used to make a court-ordered payment to a divorced spouse, child, or dependent. Other exemptions are defined by the IRS.

Read up on the IRS website, ask your HR department, and make sure you talk to someone who gets it.

401kCheckbook

Accuplan

Advanta IRA

American Estate & Trust

American IRA

American Pension Services (defunct)

American Trust Retirement

Asset Exchange Strategies

Broad Financial

Cambridge Retirement Services

CamaPlan

Capital IRA

Central Bank (may not currently support self-directed IRAs)

Checkbook IRA

Community National Bank

Crowdfund IRA

Digital Trust Company

The Entrust Group

Equity Institutional

Equity Trust Company

First Trust Company of Onaga

Financial Trust Company

Forge Trust Company (formerly IRA Services Trust Company)

GoldStar Trust Company

Guidant Financial Group, LLC

Horizon Trust Company

iPlanGroup

IRA Advantage

IRA Club

IRA Express, Inc.

IRA Financial Group

IRA Innovations

IRA Resources (merged with New Direction Trust Company)

IRA Services Trust Company (merged with Forge Trust)

IRAvest

Kingdom Trust Company

Lincoln Trust Company (now part of Millennium Trust Company)

Madison Trust Company

Mainstar Trust

Midland IRA

Millennium Trust Company

Mountain West IRA

MyEquity IRA

Nevada Trust Company

New Direction IRA (now New Direction Trust Company)

New Standard IRA

Next Generation Trust Services

Nexus Direct IRA

NuView IRA

Pacific Premier Trust (formerly PENSCO)

Peak Trust Company

PGI Agency

PolyComp Trust Company

Preferred Trust Company

Premier Trust

Provident Fiduciary Trust

Provident Trust Group

Quest Trust Company (formerly Quest IRA)

RealTrust IRA Alternatives

Safeguard Advisors

Self Directed

Self Directed IRA Services, Inc. (merged with Mainstar Trust)

Sense Financial

Sovereign International Pension Services

Specialized IRA Services

Summit Trust Company

SunWest Trust Company

The Self-Directed IRA Graveyard

Trust Company of America (acquired by ETRADE and now ETRADE Advisor Services)

uDirect IRA

Vantage

If you would like a referral to the teams that we use please click this button, complete the form, and we will be in contact with in 2-3 business days.

QRPs or qualified retirement plans (Solo 401ks, checkbook IRAs, etc) are the answer to that person with a bunch of money in their existing 401K or IRA.

It’s pretty typical that someone listens to the Wealth Elevator podcast, signs up for the investor club, and books a free intro call, has $500k+ locked up in garbage retail investments, AKA 401K.

Stop! Whatever you do, don’t roll-over an old employer’s 401K into your current employer’s 401K. If you have money in your current employer’s 401K, it’s stuck there. You need to quit your job. Well, there is this one obscure tactic if you live in a red state that could work… but for you, it’s easier to take a loan from the existing 401K to start investing in hard assets.

Anyways, let me know if you would like a referral to my checkbook IRA contact. Join the club!

"If your income is under 340K, and/or your IRA/QRP/Retirement funds is under 500k, and/or you are less than 55 years old, I think dumping your IRA/QRP money (in a controlled manner, managing your AGI not going too high) is the way to go."

Lane Kawaoka

If you are conservatively using prudent leverage and finding decent deals, there is no reason you should not be able to retire in 10 years or less, and thus negating the very reason for these accounts that you can’t touch till you are old.

When you have money in these accounts, it sounds good that you are not taxed on gains, but you are restricted from getting a Fannie Mae loan. Using SDIRA’s, you have to get second tier financing options because its more risk for the bank. For example, a Roth IRA can buy real estate on leverage, however, will need a non-recourse loan, which is often a fraction high-interest rate and lower LTV. No Bueno!

Caveat: If you are late to the game and already have a 401k over $500,000+, then you should convert it to a solo401k. At that point, you should think about putting it into a syndication since you are restricted on how you can leverage it.

I work with people to come up with a strategy to withdraw their 401k to minimize taxes. Sometimes we need to get creative with oil & gas investments, land conservation easements, or bonus depreciation.

Let’s say you choose to make an early 401k withdrawal of $100,000. (Your personal tax bracket will be different):

Technically you can get a early withdrawal, but withdrawals made under the age of 59½ will only not be subject to the 10% early withdrawal tax under the following circumstances:

What is the largest source of Revenue for the US IRS?

401K, SDIRA, IRAs, even Roth’s when not if they can change the tax laws. Basically, qualified retirement money.

"I agree that retirement plans are bad. When you contribute to a 401K, IRA or other deferred compensation plan, you are voluntarily giving the IRS a tax lien on all of the retirement money and the growth on that money. Also, with tax rates likely to be higher in the future, the amount of the tax lien will increase."

HUI Club Investor

This is my order of contributing to these (future money) accounts, after you take of (today money) regular liquidity.

[I suggest per hour coaching]:

1st QRP – contribute at least until the match.. 100% return (that said this company match things in pretty negligible amount)

2nd IRA – Flexibility to self-direct

3rd SERP – liability of the employer… pays out when you leave or after retirement age or a designated age in the future

There are a couple caveats to point out:

Answer [Note: From CPA and not this is NOT legal or professional advice]: When you invest in a business (syndicate = business) with your IRA, the IRA will be subject to UBIT (unrelated business income tax) and UDFI (unrelated debt-financed income).

For our purposes, UDFI is produced when an IRA uses debt to purchase real estate. Essentially, the portion of the property’s income considered UDFI is based on the percentage of rental income derived from debt.

For example, Property A is purchased for $100,000. You put down 25% of the purchase price as a down payment and finance the remaining 75% with a traditional mortgage from the bank. The property produces $10,000 in net income for the year. $7,500 (75%) of the net income is considered UDFI and is subject to UBIT.

There is a deduction for the first $1,000 of income subject to UBIT. Income subject to UBIT over $1,000 is taxed at trust rates. For 2017, trust tax rates start at 15% and max out at 39.6% after just $12,400 of income subject to UBIT.

UBIT is paid by the IRA account. If for whatever reason UBIT is paid directly by the taxpayer, the amount paid is considered a contribution to the IRA.

Follow up question: Is there any difference in how the UDFI will apply for these:

1) SD IRA

2) SEP-IRA

3) Solo 401K

4) SD IRA (operated as an LLC) so this one is confusing… My LLC owns an LLC (syndication) which owns a property such as 150-unit on 123 main street

But also remember – if you are in a deal that is doing a cost segregation (often 40-80% of what you put in as passive losses in the first year alone) then the UDFI gains should essentially be wiped out. 😁 So something to consider.

Answer: The solo 401(k) is not subject to UDFI but it subject to UBIT. The IRAs are all subject to UBIT and UDFI. Note that generally the passive income flowing back to you is very low and the, as a result, we don’t see a huge UBIT tax.

Another idea would be to take a debt position (lending) rather than equity. The interest you would receive is free of UBIT and UDFI tax.

(This suggestion of a “debt” position or note investment with the SEP IRA to avoid UBIT and UDFI tax is a creative one… but it’s a very low chance of happening because it’s just too complicated and honestly not worth the effort from the syndicators’ side. It’s a very similar case of to a Tenant-In-Common (TIC) arrangement where an investor has 1031 exchange funds and wants to parlay that money into a syndication. It’s possible but from the syndicator’s perspective a lot of unneeded work when you can just raise the funds the traditional way. Caveat: if you are bringing in a huge amount of money say 50% of the raise then that might tip the scales in your favor)

Ask you can tell this is a really grey area. One CPA mentioned, the answer depends on how you structured the syndication, UBIT may or may not apply for the real estate holding for solo 401k. I would really try to toss the Operation Agreement to your individual CPAs to examine and determine ahead of time as I am not a CPA 😉

Caveat: If you are late to the game and already have a fat 401k then you should convert it to a solo401k. At that point, you should think about putting it into a syndication since you are restricted on how you can leverage it.

So if you are going to have one of these QRP accounts since you have an old 401K or old retirement accounts want to self-direct it in good investments and don’t want to take a huge tax hit right away set up a Solo401k or SDIRA.

“Hey Lane! I asked my CPA [who actually knows what they are doing… let me know if you want a referral] and here is what they said…” [my additions]

Converting Roth IRA into Traditional IRA is called “Recharacterization”. It is not as common as Traditional IRA –> Roth IRA, due to the tax benefit of Roth IRA.

In 2018, as part of the Tax Cut and Jobs Act, recharacterization of Roth IRA conversions from traditional IRAs and qualified plans (e.g., 401(k)) was repealed. As a result, all Roth conversions taking place on or after January 1, 2018 are irrevocable. But recharacterizing Roth contributions is still permitted. For instance, a traditional IRA contribution can be recharacterized to a Roth IRA contribution and vice-versa.

Prior to January 2018, an investor had four available recharacterization options including: (1) traditional IRA contribution to a Roth IRA, (2) Roth IRA contribution to a traditional IRA, (3) conversion of traditional, SEP, or SIMPLE IRA and (4) qualified plan (e.g., 401(k)-to-Roth IRA conversion to a traditional IRA). Under the new rules, the list of options has been reduced.

According to the IRS, a Roth IRA conversion made in 2017 may be recharacterized as a contribution to a traditional IRA if the recharacterization is made by October 15, 2018. A Roth IRA conversion made on or after January 1, 2018, cannot be recharacterized, the IRS says. For details, see “Recharacterizations” in Publication 590-A, “Contributions to Individual Retirement Arrangements (IRAs).”

See how the government took money from Americans in the SECURE Act here.

I have been having a lot of calls with listeners having exhausted their liquidity and have money in their 401K or IRA’s still in Wall Street Investments.

One of those ways to get the money out is via a QRP or Solo401K.

I cashed out my 401k because I figured I was going to pay the taxes anyway and my tax load would be a lot higher in the future and I wanted access to my money before retirement age.

My name is Lane Kawaoka, and I hope my blog/podcast will help families realize the powerful wealth-building effects of real estate so they can spend their time on more important, instead of working long hours and worrying about their financial troubles. There are a lot of successful families with good jobs (teachers / engineers / programmers / finance) yet they struggle to make ends meet financially. It is their kiddos who ultimately get the short end of the stick. Being a Latch-Key Child growing up, both my parents had to work and I was left home alone after school to fiddle with my thumbs.

With Real Estate you are able to grow your wealth exponentially faster than the conventional 401K’s and stock investing, therefore you are able to escape the dogma of working 50+ hour weeks at a job that is unfulfilling. And if you are one of the lucky ones who happen to do what you enjoy… well good for you 😛

Money is not everything but it is important because it gives you the freedom to live life on your terms.

Annoyed by the bogus real estate education programs out there (that take money from people who don’t have it in the first place), I set out to make this free website to help other hard-working professionals, the shrinking middle-class. I hope to dispel the Wall-Street dogma of traditional wealth-building, and offer an alternative to “garbage” investments in the 401K/mutual funds that only make the insiders rich. We help the hard-working middle-class build real asset portfolios, by providing free investing education, podcasts, and networking, plus access to investment opportunities not offered to the general public.

“The true meaning of wealth is having the freedom to do what you want, when you want, and with whom you want.

Building cash flow via real estate is the simple part. The difficult part occurs after you are free financially to find your calling and fulfillment.

But that’s a great problem to have ;)”

excerpt from The One Thing That Changed Everything