Imagine this: You buy a piece of “investment-grade” art for $100,000. A year later, you donate it to a nonprofit. An appraiser—conveniently provided by the seller—claims it’s now worth $500,000. You write off the full amount as a charitable donation.

On paper, you just saved six figures in taxes. In reality, you just became an audit target.

Here’s why this tax “strategy” is dangerous—and how to avoid becoming the IRS’s next example.

The Big Idea: Art Donation as Tax Arbitrage

The strategy plays on a few key points in the tax code:

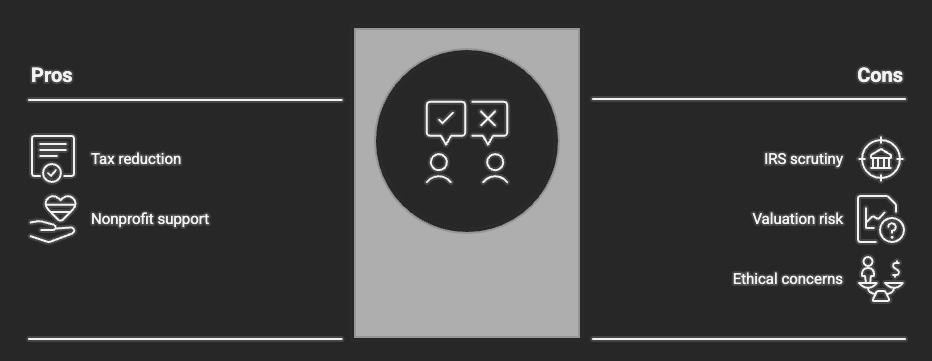

- Donated assets can be written off at fair market value

- If held over a year, they qualify for long-term capital gains treatment

- Charitable contributions reduce your AGI (with some limits)

So the pitch goes like this:

- Buy a $100K piece of art (from their “curated” collection)

- Hold it 12+ months

- Use their in-house appraiser to value it at $400K–$500K

- Donate it to a nonprofit and deduct the full appraised value

The marketer makes it sound turnkey: “You don’t need to know anything about art. We handle it all.”

And that’s exactly the problem.

Why It Matters Now

This strategy is officially on the IRS’s Dirty Dozen list—an annual roundup of the most abusive tax schemes under increased scrutiny.

As more high-income earners try to optimize taxes, these “too good to be true” plays are gaining traction. But the IRS is responding with audits, disallowed deductions, valuation penalties, and worse.

We’re seeing tighter enforcement around valuation-based deductions and increased focus on charitable donation abuse. If you’re a high net worth individual looking to reduce taxes, it’s critical to understand where smart planning ends—and risk begins.

Real-World Case Study: A Near Miss

A client of ours was pitched this exact strategy. They were excited: “I buy the art, donate it in a year, and get a 5X deduction. The consultant said they’ll even handle everything.”

I asked a few questions:

- “Can I see the appraisal methodology?”

- “Who is the appraiser?”

- “What comps are they using?”

Silence. That was our answer. The client walked away—thankfully—before it became a massive tax headache.

If they hadn’t, here’s what would’ve happened during an audit:

- The IRS sees the $100K purchase, and the $500K deduction 12 months later

- They question the appraisal, comps, and credentials

- If they find the numbers inflated, they disallow the deduction

- The investor owes back taxes, interest, and penalties

This isn’t hypothetical. We’ve seen cases where valuations are disqualified, triggering penalties under IRC §6662—which allows for 20%+ fines just on valuation overstatements.

Mistakes to Avoid / Myths to Bust

- Mistake #1: Thinking turnkey = safe.

If someone else is doing everything for you, guess who the IRS holds accountable when things go south? You. - Mistake #2: Believing one appraisal is enough.

A “friendly” appraiser doesn’t help your case. In fact, it makes it worse if there’s bias or inflated comps. - Myth: “Everyone’s doing it — it must be fine.”

The IRS is cracking down specifically because this has gotten popular. That’s not validation — that’s a warning sign.

How to Apply This

There’s nothing wrong with charitable giving. But if you want to claim a deduction, follow these guidelines:

- Don’t buy the asset solely for the deduction. Intent matters.

- Get a third-party, arms-length appraisal from someone who doesn’t benefit from the transaction.

- Ask your CPA to review the structure before you buy anything.

- If you wouldn’t feel comfortable defending it in an audit