A lot of successful investors eventually get around to estate planning.

You meet with the attorney. You set up the trust. You name the beneficiaries. You pick a trustee. Maybe you even move assets into an irrevocable trust because your estate has grown, your kids are getting older, or you are starting to think seriously about legacy.

Then the binder goes on the shelf.

And most people think, “Okay, I handled it.”

But here is the issue I see with a lot of first-generation wealth builders: the trust may answer where the money goes, but it often does not explain what the money is for.

That is where a letter of wishes comes in.

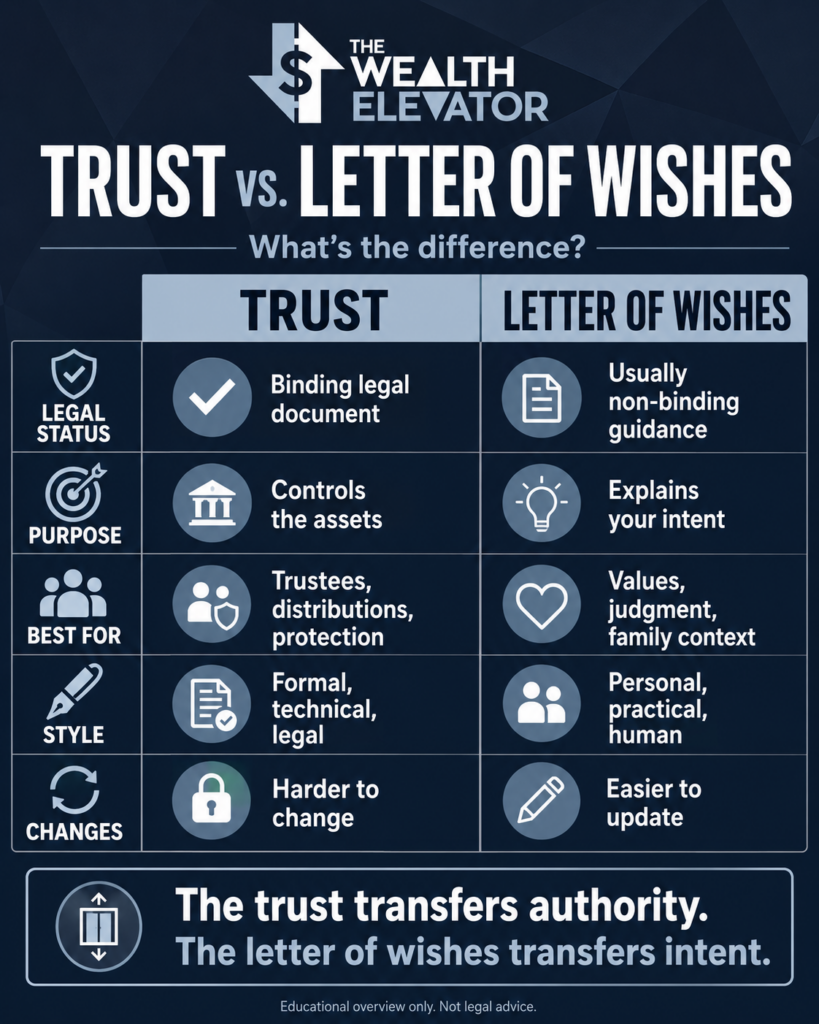

A trust is generally a fiduciary structure where a trustee holds or manages property for the benefit of beneficiaries. The trustee has duties to act in the beneficiaries’ interest. :contentReference[oaicite:0]{index=0} A letter of wishes, on the other hand, is generally a non-binding companion document that gives trustees guidance about your preferences, values, and intentions. :contentReference[oaicite:1]{index=1}

Simple translation: the trust transfers authority. The letter of wishes transfers intent.

That second part matters more than people think.

Section 1 — The Big Idea

A letter of wishes is not usually the legal document that controls the assets. That is the trust’s job.

The trust might say something like:

“The trustee may distribute income or principal for health, education, maintenance, and support.”

That sounds fine until real life shows up.

Does “education” mean college only? What about trade school? A coding bootcamp? Financial literacy training? A business mentorship program? Therapy after a bad divorce? A career pivot at age 38?

Does “support” mean helping with a first home? Paying rent forever? Covering private school for grandkids? Helping a child who chose a lower-paying career in public service? Funding a business idea?

Those are not always legal questions. A lot of times, they are judgment questions.

And the person answering those questions may not be you.

It may be an auntie.

An uncle.

A sibling.

A close friend.

A professional trustee.

That person may love your kids. They may be honest. They may have good intentions. But they may not know how you think about work, struggle, contribution, lifestyle, family, and money.

That is the gap a letter of wishes can help fill.

It is not meant to control everyone from the grave. It is meant to give the trustee a practical operating manual for gray-area decisions.

Section 2 — Why It Matters Now

A lot of people in their 40s, 50s, and 60s are dealing with a newer problem: they have created more wealth than they grew up with.

That sounds like a good problem, and in many ways it is. But it creates a parenting and legacy challenge.

If you are a first-generation millionaire, you probably built your wealth through some combination of W-2 income, business ownership, real estate, tax strategy, risk-taking, delayed gratification, and probably a few painful mistakes.

Your kids may only see the finished product.

They see the house.

The trips.

The investment accounts.

The flexibility.

They may not see the crappy first job, the years of grinding, the bad deals, the tenants, the mistakes, the stress, or the uncomfortable risks that built the family balance sheet.

So when the trust eventually starts distributing income, the next generation can confuse family capital with personal capability.

That is where the letter of wishes becomes valuable.

It gives you a place to say:

- We are okay helping you build a meaningful life.

- We are not trying to remove your need to work, contribute, and develop judgment.

- We want this money to be a trampoline, not a hammock.

That last phrase is important.

If a kid steps onto inherited wealth and brings no effort, no discipline, and no direction, they can actually sink lower. But if they bring effort, skills, and purpose, the wealth can help them jump higher.

That is the goal.

Not entitlement.

Not fake scarcity.

Not pretending the money does not exist.

And not dumping a pile of money on someone who has never had to make decisions with it.

Section 3 — Real-World Example or Case Study

Here is a simple example.

Let’s say a family has $8 million in investable assets and creates an irrevocable trust for the kids. The trust gives the trustee discretion to distribute for health, education, maintenance, and support.

Sounds reasonable.

But now fast-forward 15 years.

One child wants $150,000 to start a business.

Another wants help with a down payment on a $1.5 million house.

Another chose a lower-paying career in teaching or nonprofit work and wants supplemental income.

Another does not need money but feels distributions should be “equal.”

The trustee is an uncle.

He loves the kids. He wants to keep peace in the family. He does not want to be the bad guy at Thanksgiving. But he is also a fiduciary and has to make decisions in the best interest of the beneficiaries. Trustees generally owe fiduciary duties when managing trust assets for beneficiaries. :contentReference[oaicite:2]{index=2}

Without a letter of wishes, the uncle is guessing.

With a strong letter of wishes, he has guidance.

For example, the letter could say:

“We are comfortable helping with a first home, but we prefer the beneficiary to have stable income, some personal savings, and a purchase that does not require permanent family subsidies.”

“If a beneficiary wants capital for a business, we prefer staged funding tied to milestones, a basic written plan, and evidence that the beneficiary has meaningful personal commitment.”

“We support meaningful work that may not pay highly, including education, public service, ministry, caregiving, nonprofit work, or community work. However, we do not want the trust to replace personal responsibility or create permanent lifestyle dependence.”

“Fair does not always mean equal. Please consider maturity, purpose, need, and whether the distribution helps the beneficiary grow.”

That is useful.

It gives the trustee a framework.

It also helps reduce family drama because the trustee can point back to your stated intent instead of making every decision feel personal.

Section 4 — Mistakes to Avoid / Myths to Bust

Mistake #1: Thinking the trust document explains your values.

Most trust documents are written in legal language. That is not a criticism. That is their job.

But your kids and future trustee may need more than legal language. They may need to understand how you define support, responsibility, work, education, entrepreneurship, community, and stewardship.

The trust may say what is allowed.

The letter of wishes explains what is wise.

Mistake #2: Saying “just use your best judgment.”

This sounds reasonable, but it can create problems.

Your trustee’s best judgment may not be your judgment.

This is especially true if the trustee is a family member. Auntie or uncle may be emotionally close to the kids. They may not want conflict. They may feel pressure to say yes. Or they may overcorrect and become too rigid.

The letter of wishes helps them understand the difference between helping and enabling.

Mistake #3: Trying to control every future decision.

A letter of wishes should not become a second trust document.

It should not contradict the trust. In general, letters of wishes are guidance and should not conflict with the trust terms or attempt to override the trust document. :contentReference[oaicite:3]{index=3}

Avoid language like:

- “Trustee must always…”

- “Never allow…”

- “Make sure my kids never struggle…”

- “Maintain the lifestyle they grew up with…”

Better language sounds like:

- “Our hope is…”

- “Our preference is…”

- “In exercising your discretion, please consider…”

- “We would view this type of support as consistent with the purpose of the trust…”

The goal is guardrails, not handcuffs.

Section 5 — How to Apply This

If you already have a trust, especially an irrevocable trust, I would not assume the planning is complete.

Here are a few questions to bring to your estate attorney:

- Does my trust give the trustee discretion?

- Would a letter of wishes be appropriate for this structure?

- Could the letter create confusion or conflict with the trust language?

- How often should I update it?

- Who should have access to it?

- How should it be stored with the trust documents?

Then think through the real-world decisions your trustee may face.

For example:

- Would you help a child buy a first home?

- Would you fund a business?

- Would you support a lower-paying but meaningful career?

- Would you pay for graduate school?

- Would you help during divorce, addiction, disability, or financial irresponsibility?

- Should distributions be equal or based on need and maturity?

- How do you define productive struggle versus unnecessary suffering?

Those are not easy questions.

But it is better to wrestle with them now than leave your trustee and kids guessing later.

Here is some sample language I like:

“We created this trust as a gift of love, not as a replacement for work, contribution, or personal responsibility.”

“We hope these resources help beneficiaries become capable, generous, healthy, and connected to family and community.”

“We are comfortable using trust resources to support education, health, career training, reasonable housing stability, entrepreneurship, and community contribution.”

“We do not want the trust to fund status, avoidance, permanent dependency, or a lifestyle that requires ongoing subsidies.”

“Please use discretion in a way that builds judgment over time.”

That is the essence of a good letter of wishes.

It does not try to predict every future scenario.

It gives the trustee a compass.

Conclusion

A trust is important.

But a trust by itself may not be enough.

Especially if you are trying to pass down more than assets.

Most of us do not want to raise kids who are rich on paper but poor in judgment.

We want the next generation to understand the difference between money they earned and money the family trust provides. We want them to build competence through time, work, mistakes, and responsibility. We want wealth to strengthen community and ohana, not isolate them.

That is why a letter of wishes can be so useful.

The trust tells the trustee what they can do.

The letter of wishes helps explain what you hoped they would do.

One transfers authority.

The other transfers intent.

And when the trustee is no longer you, that intent may be one of the most valuable things you leave behind.

Educational overview only. This is not legal advice. Work with a qualified estate attorney in your state before drafting or changing any trust-related documents. Please let us know if you need a referral to 💼 CPA ⚖️ Lawyer or other vendor here.