ATM Background

Let’s delve into the realm of automated teller machines (ATMs).

While many of us simply swipe our cards and withdraw cash without a second thought, there’s a whole world of intricacies behind the scenes. This includes the languages they communicate in, the alliances they form, and the complex web of fees involved at every level.

If you’ve ever been curious about the economics and inner workings of ATMs, or if you’re interested in investing in them, this edition is tailored for you.

Discover:

– The origins of the ATM.

– The rapid expansion of ATMs.

– How lesser-known ATMs establish communication with your bank.

– Insight into Electronic Funds Transfer (EFT) networks.

– The major EFT networks that fly under the radar.

– The revenue model behind surcharge-free ATMs.

– The concept of ATM alliances.

– Leading companies in the ATM alliance space.

– Investment opportunities in the ATM sector.

– Costs associated with purchasing ATM machines.

– Challenges faced in ATM investment.

– Speculations on the future of ATMs.

– Introduction to Interactive Teller Machines (ITMs) and Reverse ATMs.

– Understanding “Cashless” ATMs and their legality.

Introduction to the ATM

Let’s delve into the realm of automated teller machines (ATMs).

While many of us simply swipe our cards and withdraw cash without a second thought, there’s a whole world of intricacies behind the scenes. This includes the languages they communicate in, the alliances they form, and the complex web of fees involved at every level. If you’ve ever been curious about the economics and inner workings of ATMs, or if you’re interested in investing in them, this edition is tailored for you.

Discover:

- The origins of the ATM.

- The rapid expansion of ATMs.

- How lesser-known ATMs establish communication with your bank.

- Insight into Electronic Funds Transfer (EFT) networks.

- The major EFT networks that fly under the radar.

- The revenue model behind surcharge-free ATMs.

- The concept of ATM alliances.

- Leading companies in the ATM alliance space.

- Investment opportunities in the ATM sector.

- Costs associated with purchasing ATM machines.

- Challenges faced in ATM investment.

- Speculations on the future of ATMs.

- Introduction to Interactive Teller Machines (ITMs) and Reverse ATMs.

- Understanding “Cashless” ATMs and their legality.

Inception of the ATM

When we discuss advancements in finance, the spotlight often shines on topics like digital banking, cryptocurrencies, or innovative fundraising methods such as Regulation CF or Regulation A. However, one seemingly mundane technology has arguably wielded a more profound influence on financial services than any other: the ATM.

Since its inception in 1967, the ATM has reshaped the way people interact with banking services. It liberated individuals from the confines of traditional bank branches, enabling transactions outside of regular banking hours and locations. Today, the concept of withdrawing cash without setting foot in a physical bank seems archaic, with many individuals, myself included, having eschewed bank branches for years.

The automation of banking services and the detachment of currency from its physical origins represented a monumental shift in the financial landscape, particularly notable in the wake of the Global Financial Crisis. It prompted former Federal Reserve Chair Paul Volcker to famously remark, “The ATM has been the only useful innovation in banking for the past 20 years.”

The question of the ATM’s inventor is subject to debate. While the widely accepted narrative credits British engineer John Shepherd-Barron with the idea, reality reveals a more complex lineage. Shepherd-Barron’s bathtub epiphany, though charming, is just part of the story. The ATM’s development involved multiple projects, including the Bankograph by Luther Simjian and James Goodfellow’s patent for a PIN-based cash machine. Ultimately, Shepherd-Barron’s team installed the first modern ATM at a Barclays branch in London in 1967, marking a pivotal moment in banking history.

The proliferation of ATMs in the 1980s and 1990s was staggering. From a mere 1,500 machines globally in the early 1970s, ATMs experienced exponential growth, with a compound annual growth rate (CAGR) of 24.2% over three decades. Convenience undoubtedly played a role, but economic factors were equally significant. As societies became wealthier, cash usage declined, and electronic wage payments became the norm. Consequently, ATMs became essential conduits for accessing cash, especially in countries where cashless transactions were on the rise.

However, there are limits to this trend. In affluent societies where cash usage diminishes, the value proposition of ATMs weakens. Consequently, high-income countries have witnessed a decline in ATM numbers in recent years, reflecting broader shifts towards cashless economies.

How Do ATMs Actually Work?

The process of withdrawing cash from an ATM may seem straightforward—insert your card, input your banking details, withdraw cash, and await the deduction from your account. However, beneath this apparent simplicity lies a web of intricacies that raise several fundamental questions:

- How can you withdraw cash from an ATM belonging to a bank with which you have no account, including foreign banks while traveling?

- What enables independently owned ATMs, often not affiliated with banks, to access your bank account?

- Why do some ATMs impose surcharges for withdrawals while others do not, and how do surcharge-free ATMs sustain profitability?

- Addressing these inquiries requires a deep dive into the underlying financial infrastructure that facilitates ATM transactions, illuminating how what began as a convenient banking service has evolved into a lucrative industry of its own.

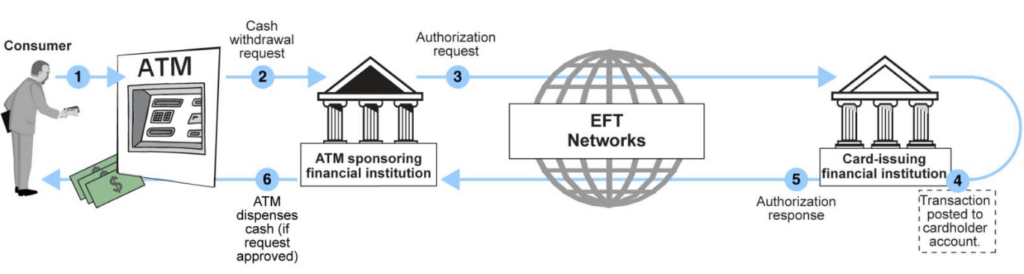

At the heart of this system are Electronic Funds Transfer (EFT) networks, which serve as the linchpin connecting banks to authenticate and verify transactions. Consider a scenario where you seek to withdraw cash from an ATM operated by a bank different from your own. Through a shared EFT network, your bank communicates with the ATM operator’s bank to confirm the availability of funds for the transaction. Upon approval, your bank disburses the cash, and settlement between the banks occurs subsequently.

The complexity escalates when dealing with non-bank ATM operators, known as Independent ATM Deployers (IADs). Since these entities lack direct access to EFT networks, they must secure sponsorship from larger banks to facilitate transactions. Consequently, when you use an IAD ATM, the sponsoring bank acts as an intermediary, relaying the transaction request through the EFT network to your bank for authorization or denial.

EFT networks serve as the universal language facilitating communication among ATMs worldwide. While banks are fluent in this language, IADs rely on sponsor banks to translate and access the network. Moreover, there exist international networks like Cirrus (owned by Mastercard) and Plus (owned by Visa), spanning the globe, alongside domestic networks tailored to specific countries or regions such as Accel, STAR, NYCE, MoneyPass, and Allpoint in North America.

For consumers, possessing a debit card bearing the Mastercard or Visa logo grants access to a vast network of ATMs worldwide, thanks to the expansive reach of Cirrus and Plus. Historically content with their role in facilitating transactions and earning fees, EFT networks have recently emerged as proponents of fee-free ATMs, reshaping the landscape of ATM accessibility.

Surcharge Fees on the Rise

The proliferation of ATM fees has elicited strong aversion from users, with nearly 80% actively seeking to avoid them. This sentiment has grown more pronounced over time, especially as ATM fees continue to climb. Consequently, offering surcharge-free ATM access has become a significant competitive advantage for banks.

Traditionally, banks furnish ATMs as a benefit to their account holders, while Independent ATM Deployers (IADs) operate ATMs as a business endeavor. Consequently, using one’s own bank’s ATM typically incurs no fees, whereas utilizing an unaffiliated ATM often results in charges.

Enter the concept of ATM alliances—a solution particularly beneficial for smaller banks unable to afford a nationwide network of proprietary ATMs. These alliances allow participating banks’ account holders to access ATMs within the network free of charge. Leveraging existing infrastructure, Electronic Funds Transfer (EFT) networks, which already interconnect banks, are ideally positioned to facilitate these alliances.

Companies like Allpoint and Moneypass, originally conceived as networks, have transitioned into owning or operating tens of thousands of fee-free ATMs across the United States. Through alliances with member banks, these networks provide widespread access to surcharge-free ATMs, collectively comprising a substantial portion of all ATMs nationwide.

Rather than directly charging users, these companies generate revenue by receiving payments from banks, typically on a per-transaction basis. Nevertheless, fee-charging ATMs persist globally, presenting potential lucrative business opportunities, particularly in prime locations.

Evolvement of ATMs

As society’s financial landscape evolves, so too do automated teller machines (ATMs), adapting to meet changing consumer needs and technological advancements.

Interactive Teller Machines (ITMs)

Acknowledging the diminishing relevance of traditional ATMs due to declining cash and check usage, some banks are embracing Interactive Teller Machines (ITMs). ITMs facilitate live video chats between customers and remote tellers, enabling more complex transactions such as loan inquiries and account openings. This innovative approach not only enhances customer service but also reduces costs for banks by potentially replacing costly domestic tellers with more economical overseas counterparts.

Reverse ATMs

In contrast to conventional ATMs where customers insert cards to withdraw cash, reverse ATMs operate in the opposite manner. Customers deposit cash into these machines and receive prepaid cards usable only at the location housing the kiosk. This solution caters to businesses seeking to accommodate cash transactions while avoiding the logistical challenges and security risks associated with handling physical currency.

Cashless ATMs

While the term “cashless ATM” may initially seem contradictory, this technology serves a unique purpose, originally emerging in the cannabis industry. Due to federal restrictions, many dispensaries struggle to process sales through traditional payment networks. Cashless ATMs offer a workaround by coding transactions as ATM withdrawals, allowing dispensaries to accept electronic payments while disguising the nature of the transaction. This method has since extended beyond the cannabis sector, with various legitimate businesses utilizing cashless ATMs to sidestep credit card processing fees.

Cash Registers as ATMs

As businesses increasingly prioritize digital payments and view cash handling as cumbersome and costly, innovative solutions are emerging to streamline transactions. One such approach involves transforming cash registers into pseudo-ATMs, offering customers the option to receive cash back during purchases, akin to the cash-back feature commonly available at grocery stores. Startups like Spare, supported by investors such as Mark Cuban, are spearheading efforts to implement this feature across a wide range of retail establishments, further blurring the lines between traditional banking and retail operations.

In essence, the evolution of ATMs reflects broader shifts in consumer preferences and technological advancements, with innovative solutions emerging to enhance convenience, efficiency, and security in financial transactions.

Investing in ATM Funds

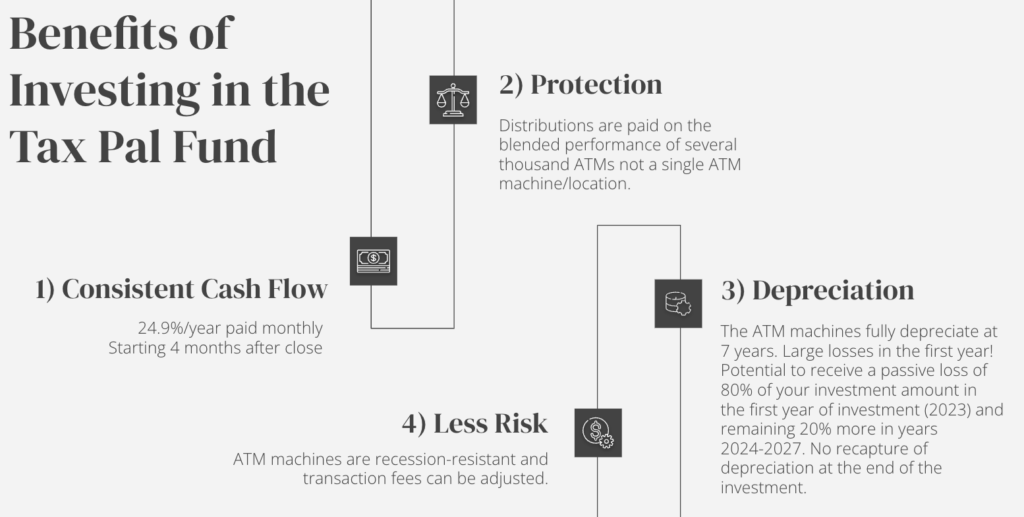

Investing in ATMs represents a prime example of real asset investing, offering ownership stakes in thousands of tangible machines. Our fund leverages the collective performance of these ATMs to mitigate volatility and offer stability, ensuring a predictable cash flow backed by real assets.

ATM investments yield a steady stream of passive income with minimal hands-on involvement, making them an attractive option for investors seeking reliable returns. Furthermore, investors benefit from favorable tax incentives associated with owning ATMs.

Depreciation from the machines is allocated to investors, resulting in significant write-offs upfront. Additionally, ATMs qualify for accelerated tax benefits through Bonus Depreciation, allowing investors to capitalize on substantial tax advantages both immediately and in subsequent years.

Investing in vetted ATM opportunities through a fund offers the quickest route for individual investors to gain exposure to this lucrative asset class. These funds consist of thousands of ATM machines strategically spread across different locations, providing instant diversification in terms of quantity and geography.

Participating in an ATM fund involves solely investing capital, with no operational responsibilities or obligations, rendering it a fully passive investment. Typically, ATM funds have predefined investment horizons, such as seven years, and distribute returns to investors on a monthly or quarterly basis.

ATM investing offers several compelling benefits:

- Large and expanding user base.

- Relatively stable monthly transaction volume.

- Potential for consistent cash flow, albeit not guaranteed.

- Potential for returns that surpass those of other investment vehicles.

- Tax benefits related to depreciation, owing to the shorter lifespan of ATMs compared to real estate.

- Resilience to economic downturns compared to other investments, as ATMs are non-correlated assets.

- Portfolio diversification for investors.

begin your journey to financial freedom!

My name is Lane Kawaoka, and I hope my blog/podcast will help families realize the powerful wealth-building effects of real estate so they can spend their time on more important, instead of working long hours and worrying about their financial troubles. There are a lot of successful families with good jobs (teachers / engineers / programmers / finance) yet they struggle to make ends meet financially. It is their kiddos who ultimately get the short end of the stick. Being a Latch-Key Child growing up, both my parents had to work and I was left home alone after school to fiddle with my thumbs.

With Real Estate you are able to grow your wealth exponentially faster than the conventional 401K’s and stock investing, therefore you are able to escape the dogma of working 50+ hour weeks at a job that is unfulfilling. And if you are one of the lucky ones who happen to do what you enjoy… well good for you 😛

Money is not everything but it is important because it gives you the freedom to live life on your terms.

Annoyed by the bogus real estate education programs out there (that take money from people who don’t have it in the first place), I set out to make this free website to help other hard-working professionals, the shrinking middle-class. I hope to dispel the Wall-Street dogma of traditional wealth-building, and offer an alternative to “garbage” investments in the 401K/mutual funds that only make the insiders rich. We help the hard-working middle-class build real asset portfolios, by providing free investing education, podcasts, and networking, plus access to investment opportunities not offered to the general public.

“The true meaning of wealth is having the freedom to do what you want, when you want, and with whom you want.

Building cash flow via real estate is the simple part. The difficult part occurs after you are free financially to find your calling and fulfillment.

But that’s a great problem to have ;)”

excerpt from The One Thing That Changed Everything